File C3-25

FM 1816 Revised July 2021

Ag Decision Maker

Your Farm

Income Statement

How much did your farm business earn last year?

Was it profitable? There are many ways to answer

these questions.

A farm income statement (sometimes called a

profit and loss statement) is a summary of income

and expenses that occurred during a specified

accounting period, usually the calendar year for

farmers. It is a measure of input and output in

dollar values. It offers a capsule view of the value

of what your farm produced for the time period

covered and what it cost to produce it.

Most farm families do a good job of keeping

records of income and expenses for the purpose

of filing income tax returns. Values from the tax

return, however, may not accurately measure the

economic performance of the farm. Consequently,

you need to have a clear understanding of the

purpose of an income statement, the information

needed to prepare the statement, and the way in

which it is summarized.

Net farm income, as calculated by the accrual or

inventory method, represents the economic return

to your contributions to the farm business: labor,

management, and net worth in land and other

farm assets. Cash net farm income also can be

calculated. It shows how much cash was available

for purchasing capital assets, debt reduction,

family living, and income taxes.

Preparing the Statement

The income statement is divided into two parts:

income and expenses. Each of these is further

divided into a section for cash entries and a section

for noncash (accrual) adjustments.

An example income statement is shown at the end

of this publication, along with a blank form. Blank

forms for developing your own income statement

are also available in ISU Extension and Outreach

publication FM 1824, AgDM C3-56: Farm

Financial Statements, https://store.extension.

iastate.edu/Product/1827.

Most of the information needed to prepare an

income statement can be found in common farm

business records. These include a farm account

book or program, Internal Revenue Service

(IRS) forms 1040F Profit or Loss From Farming

and 4797 Sales of Business Property, and your

beginning and ending net worth statements for

the year. If you use the IRS forms, you will need to

organize the information a bit differently to make

allowances for capital gains treatment of breeding

stock sales and the income from feeder livestock or

other items purchased for resale.

Cash Income

Cash income is derived from sales of livestock,

livestock products, crops, government payments,

tax credits and refunds, crop insurance proceeds,

and other miscellaneous income sources.

• Include total receipts from sales of both raised

livestock and market livestock purchased for

resale. Remember not to subtract the original

cost of feeder livestock purchased in the

previous year, even though you do this for

income tax purposes. Also include total cash

receipts from sales of breeding livestock before

adjustments for capital gains treatment of

income are made. These are termed “gross sales

price” on IRS Form 4797.

• Do not include proceeds from outstanding

USDA marketing loans in cash income even if

you report these as income for tax purposes.

• Do not include noncash income such as profits

or losses on futures contracts and options.

However, do include cash withdrawn from

hedging accounts.

• Do not include sales of land, machinery, or

other depreciable assets; loans received; or

income from nonfarm sources of income.

Page 2

Your Farm Income Statement

Adjustments to Income

Not all farm income is accounted for by cash sales.

Changes in inventory values can either increase

or decrease the net farm income for the year.

Changes in the values of inventories of feed and

grain, market livestock, and breeding livestock can

result from increases or decreases in the quantity

of these items on hand or changes in their unit

values (see Example 1). Adjusting for inventory

changes ensures that the value of farm products is

counted in the year they are produced rather than

the year they are sold. Subtract beginning of the

year values from end of the year values to find the

net adjustment.

Example 1

The beginning inventory of feeder pigs consists

of 420 head valued at $75 each, or $31,500.

Ending inventory is 450 head valued at $50

each, or $22,500. Inventory value decreased by

$9,000 even though the number of pigs on hand

increased by 30 head. The decline in value per

head more than offset the increase in numbers,

and could have been due to lower market prices

and/or lighter weight of the pigs.

Changes in the market values of land,

buildings, machinery, and equipment (except

for depreciation) are not included in the income

statement unless they are actually sold. Accounts

receivable and unpaid patronage dividends are

included, however, because they reflect income

that has been earned but not yet received.

Cash Expenses

All cash expenses involved in the operation of the

farm business during the business year should be

entered into the expense section of the income

statement. These can come from Part II of IRS

Schedule F. Under livestock purchases include

the value of breeding livestock as well as market

animals.

• Do not include death loss of livestock as an

expense. This will be reflected automatically by

a lower ending livestock inventory value.

• Income tax and Social Security tax payments are

considered personal expenses and should not be

included in the farm income statement, unless

the statement is for a farm corporation.

• Interest paid on all farm loans or contracts is a

cash expense, but principal payments are not.

• Do not include the purchase of capital assets

such as machinery and equipment. Their cost

is accounted for through depreciation. Land

purchases also are excluded.

• You may wish to exclude wages paid to family

members because these also are income to

the family.

• Include cash deposits made to hedging

accounts.

Adjustment to Expenses

Some cash expenses paid in one year may be

for items not actually used until the following

year. These include feed and supply inventories,

prepaid expenses, and investments in growing

crops. Subtract the ending value of these from the

beginning value to find the net adjustment (see

Example 2).

Example 2

Beginning inventory of fertilizer was zero.

Closing inventory is worth $11,000. Fertilizer

purchases during the year were $16,000, all paid

for. The change in inventory is a positive $11,000.

Even though $16,000 is shown for cash expense,

only $5,000 ($16,000 − $11,000) is charged to

the farm operation during the year covered.

The $11,000 of fertilizer still unused will be the

beginning inventory value for the following year,

and will be included in that year’s expenses.

Other expenses may be incurred in one year but

not paid until the following year or later, such

as farm taxes due, and other accounts payable.

Record accounts payable so that products or

services that have been purchased but not paid for

are counted. However, do not include any items

that already appear under cash expenses. Subtract

the beginning total of these items from the ending

totals to find the net adjustment. Note that interest

expense due is not included until later, after net

farm income from operations is calculated.

Page 3

Your Farm Income Statement

Depreciation is the amount by which machinery,

equipment, buildings, and other capital assets

decline in value due to use and obsolescence.

The depreciation deduction allowed on your

income tax return can be used, but you may want

to calculate your own estimate based on more

realistic depreciation rates. One simple procedure

is to multiply the value of these assets at the end of

the year by a fixed rate, such as 10%. This way you

can group similar items, such as machinery, rather

than maintain separate records for each item.

If you include breeding livestock under beginning

and ending inventories, do not include any

depreciation expense for them.

The beginning and ending net worth statements

for the farm are a good source of information

about inventory values and accounts payable

and receivable: ISU Extension and Outreach

publication FM 1791, AgDM C3-20: Your Net

Worth Statement, https://store.extension.iastate.

edu/Product/1814, provides more detail on how to

complete a net worth statement.

ISU Extension and Outreach publication FM 1824,

AgDM C3-56: Farm Financial Statements,

https://store.extension.iastate.edu/Product/1827,

contains schedules for listing adjustment items for

both income and expenses. Use the same values

that are shown on your beginning and ending net

worth statements for completing adjustments to

your net income for the year.

Summarizing the Statement

You have now accounted for cash farm income

and cash expenses (excluding interest). You also

have accounted for depreciation and changes

in inventory values of farm products, accounts

payable, and prepaid expenses. You are now ready

to summarize two measures of farm income.

Net Farm Income from Operations

Subtract total farm expenses from gross farm

revenue. The difference is the net income

generated from the ordinary production and

marketing activities of the farm, or net farm

income from operations.

Interest Expense

Interest is considered to be the cost of financing

the farm business rather than operating it.

Net interest expense is equal to cash interest

expense adjusted for beginning and ending

accrued interest.

Capital Gains and Losses

Some years income is received from the sale

of capital assets such as land, machinery, and

equipment. The sale price may be either more or

less than the cost value (or basis) of the asset.

For depreciable items the cost value is the

original value minus the depreciation taken.

For land it is the original value plus the cost of

any nondepreciable improvements made. The

difference between the sale value and the cost

value is a capital gain or loss. For purposes of the

farm income statement, capital gain would also

include the value of “recaptured depreciation”

from the farm tax return. Information for

calculating capital gains and losses can come from

the depreciation schedule or IRS Form 4797.

Sales of breeding livestock can be handled two

ways: (1) record sales and purchases as cash

income and expenses, and adjust for changes in

inventory, or (2) record capital gains or losses

when animals are sold and include depreciation as

an expense. Either method can be used, but do not

mix them.

Net Farm Income

Subtract interest expense, then add capital gains

or subtract capital losses from net farm income

from operations to calculate net farm income.

This represents the income earned by the farm

operator’s own capital, labor, and management

ability. It also represents the value of everything

the farm produced during the year, minus the cost

of producing it.

Further Analysis

Net farm income is an important measure of the

profitability of your farm business. Even more

can be learned by comparing your results with

Page 4

Your Farm Income Statement

those for other similar farms. ISU Extension and

Outreach publication FM 1845, AgDM C3-55:

Financial Performance Measures for Iowa Farms,

https://store.extension.iastate.edu/Product/1837,

contains information about typical income levels

generated by Iowa farms. It also illustrates other

important measures and ratios that can help you

evaluate the profitability, liquidity, and solvency

of your own business over time.

Other Financial Statements

Two other financial statements are often used

to summarize the results of a farm business.

While they are not as common as the net income

statement and the net worth statement, they do

provide useful financial information.

Statement of Cash Flows

A statement of cash flows summarizes all the cash

receipts and cash expenditures that were received

or paid out during the accounting year. It is

sometimes called a flow of funds statement. Unlike

the net income statement, it does not measure the

profitability of the business. It merely shows the

sources and uses of cash. The statement of cash

flows is divided into five sections:

• cash income and cash expenses

• purchases and sales of capital assets

• new loans received and principal repaid

• nonfarm income and expenses (sole proprietor)

• beginning and ending cash on hand

If all cash flows are accurately recorded, the

total sources of cash will be equal to the total

uses of cash. If a significant difference exists,

the records should be carefully reviewed for

errors and omissions.

An example of a statement of cash flows is

found at the end of this publication, along

with a blank form.

Statement of Owner Equity

The statement of owner equity ties together

net farm income and the change in net worth.

Net worth will increase or decrease during the

accounting year based on three factors:

• net farm income (accrual)

• net nonfarm withdrawals (nonfarm income

minus nonfarm expenditures)

• adjustments to the market value of capital assets

(affects market value net worth only)

If these factors are recorded accurately and added

to the beginning net worth of the farm, the result

will equal the ending net worth.

An example of a statement of owner equity is

found at the end of this publication, along with a

blank form.

Further resources on financial information can be

found on the Ag Decision Maker website, www.

extension.iastate.edu/agdm/wdfinancial.html.

• Decision Tool C3-26, Cash to Accrual Net

Farm Income Worksheet, www.extension.

iastate.edu/agdm/wholefarm/xls/

c3-26accrualnfi.xlsx

• Decision Tool C3-56, Comprehensive

Financial Statements, www.extension.

iastate.edu/agdm/wholefarm/xls/c3-

56comprfinstatements.xlsx

This institution is an equal opportunity provider.

For the full non-discrimination statement or

accommodation inquiries, go to www.extension.

iastate.edu/diversity/ext.

Prepared by William Edwards,

retired extension economist

www.extension.iastate.edu/agdm

store.extension.iastate.edu

Page 5

Your Farm Income Statement

Net Farm Income Statement Example

Name

Cyclone Farm

Year

2019

Income

Cash Income (numbers in ( ) refer to IRS Schedule F) Income Adjustments Beginning Ending

Sales of livestock bought for resale (1a)

$423,735

Hedging accounts balance

$41,500 $47,909

Sales of raised livestock, grain, etc. (2)

451,028

Crops held for sale or feed

538,150 489,105

Cooperative distributions paid (3a)

4,280

Market livestock

296,160 329,403

Agricultural program payments (4a) Accounts receivable

15,445

Crop insurance proceeds (6a) Unpaid cooperative distributions

24,581 28,861

Custom hire income (7)

8,740

Breeding livestock

201,000 222,600

Other income (8), cash only

2,563

Other current assets

Sales of breeding livestock

5,680

Subtotal of income adjustments

$1,116,836 $1,117,878

Hedging accounts withdrawals

3,000

b. Net income adjustment (ending − beginning)

$1,042

a. Total Cash Income

$899,026

c. Gross Farm Revenue (a + b)

$900,068

Expenses

Cash Expenses (numbers in ( ) refer to IRS Schedule F) Expense Adjustments (paid in advance) Beginning Ending

Car and truck expenses (10) Investment in growing crops

$13,040 $8,680

Chemicals (11)

$18,456

Commercial feed on hand

10,000 10,940

Conservation expenses (12) Prepaid expenses

20,387 0

Custom hire (13)

9,589

Supplies on hand

14,500 2,000

Employee benefits (15) Subtotal of adjustments

$57,927 $21,620

Feed purchased (16)

179,150

e. Net adjustment (beginning − ending)

$36,307

Fertilizer and lime (17)

75,890

Expense Adjustments (due) Beginning Ending

Freight, trucking (18)

15,690

Farm accounts payable

$4,589 $1,859

Gasoline, fuel, oil (19)

11,899

Farm taxes due

4,400 4,750

Insurance (20)

18,913

Subtotal of adjustments (expenses due)

$8,989 $6,609

Interest paid (21a + 21b)

25,442

f. Net adjustment (ending − beginning)

($2,380)

Labor hired (22)

13,654

g. Depreciation

$53,150

Pension and profit-share plans (23) h. Total Operating Expenses (d + e + f + g)

$808,152

Rent or lease payments (24a + 24b)

125,600

(excluding interest)

Repairs, maintenance (25)

13,136

i. Net Farm Income from Operations (c − h)

$91,916

Seeds, plants (26)

56,800

Interest Adjustments Beginning Ending

Storage, warehousing (27) Accrued interest

23,725 22,484

Supplies purchased (28)

4,890

j. Net interest expense

$24,201

Taxes (farm) (29)

8,800

(cash − beginning + ending)

Utilities (30)

4,629

Total Farm Expenses (h + j)

$832,353

Vet. fees, medicine, breeding (31)

6,891

k. Sales of farmland

$100,000

Other expenses (32), cash only

4,588

l. Cost value of land sold

$80,000

Livestock purchased

132,500

m. Capital gains or losses (k − l)

$20,000

Hedging accounts deposits

20,000

d. Total Cash Expenses

$746,517

n. Net Farm Income (accrual) (i − j + m)

$87,715

Net Farm Income (cash) (a − d)

$152,509

Value of Farm Production

(c − purchases of feed & livestock)

$588,418

Page 6

Your Farm Income Statement

Statement of Cash Flows Example

Name

Cyclone Farm

Year

2019

Cash In Cash Out

Cash farm income and expenses (operating)

Total cash income (line a, net farm income statement)

$899,026

xxx

Total cash expenses (line d, net farm income statement) xxx

$746,517

Capital assets (investing)

Sales of capital assets

$106,500

xxx

Cost of purchases and trades xxx

$102,000

Loans (financing)

New loans received

$446,580

xxx

Principal paid on loans xxx

$524,070

Nonfarm (withdrawals)

Nonfarm income invested in the farm business xxx

Cash withdrawn from the farm for family living, taxes, savings, etc. xxx

$69,000

Cash on hand (balance in farm checking and savings accounts, excluding hedging accounts)

Beginning of year

$6,146

xxx

End of year xxx

$16,665

Total of cash in and cash out*

$1,458,252 $1,458,252

*If all cash transactions are included correctly, the totals for the two columns will be approximately equal.

Statement of Owner Equity Example

Name_____

Cyclone Farm

____________________________________________ Year

2019

Cost Value Market Value

a. Farm net worth, beginning of year

$1,665,962 $1,820,062

(Line g, beginning net worth statement)

b. Change in market value of capital assets (net of depreciation) xxx

$148,150

(Line i, ending net worth statement, market value __$166,865__ minus cost value __$18,715___)

c. Net farm income (accrual)

$87,715 $87,715

(Line n, net farm income statement)

same value for cost and market

d. Net nonfarm withdrawals: (nonfarm income invested − cash withdrawn)

($69,000) ($69,000)

(see statement of cash flows)

same value for cost and market

e. Calculated change in net worth (b + c + d)

$18,715 $166,865

f. Farm net worth, end of year (Line g, ending net worth statement)

$1,684,677 $1,986,927

g. Actual change in net worth (f − a)

$18,715 $166,865

(line e should approximately equal line g)

h. Percent of net farm income retained in the business this year ((c + d) / c) xxx

21%

i. Percent of change in market value net worth from retained earnings this year

(g, cost value / g, market value)

xxx

11%

Page 7

Your Farm Income Statement

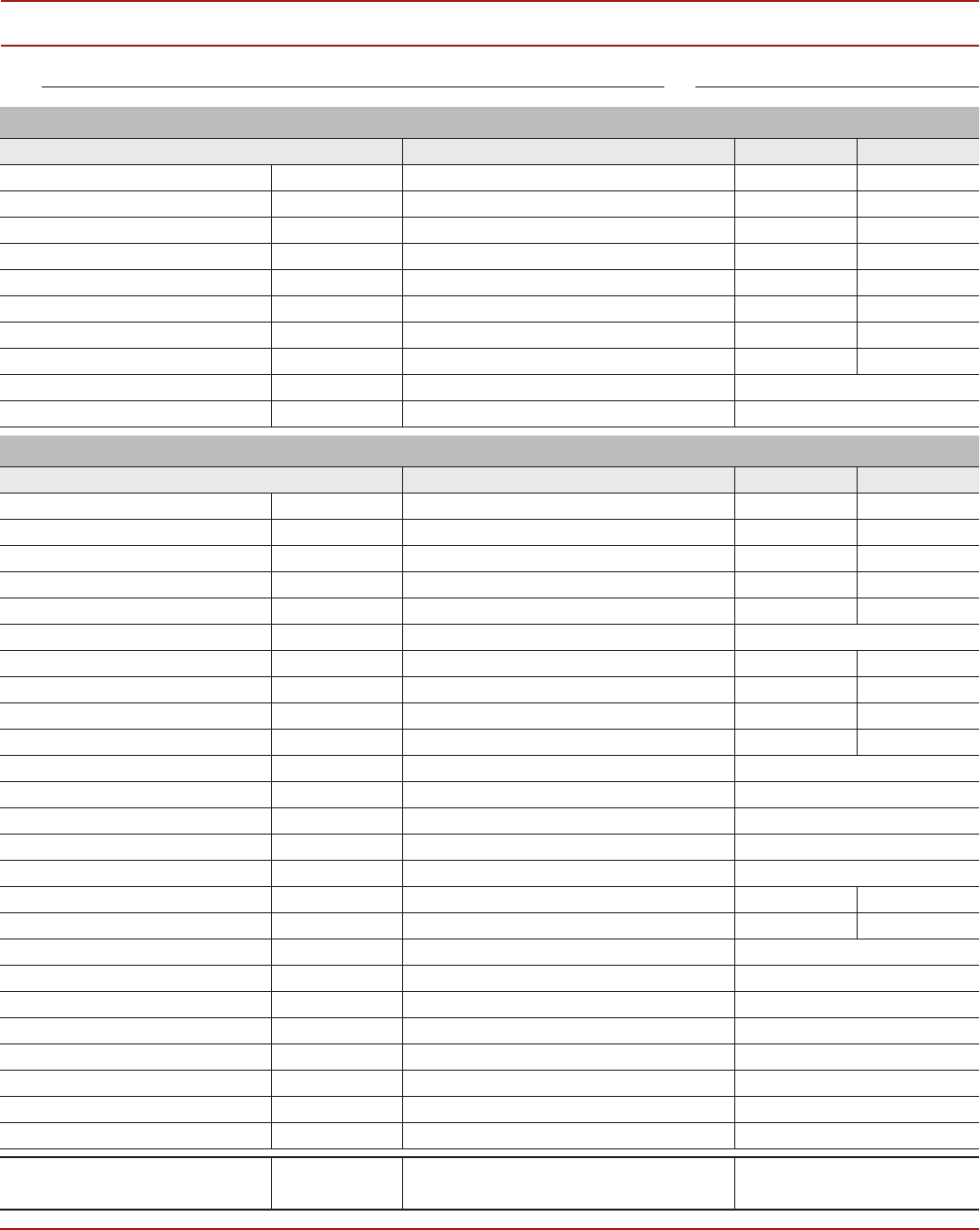

Net Farm Income Statement

Name _______________________________________________________________ Year _______________________________

Income

Cash Income (numbers in ( ) refer to IRS Schedule F) Income Adjustments Beginning Ending

Sales of livestock bought for resale (1a) Hedging accounts balance

Sales of raised livestock, grain, etc. (2) Crops held for sale or feed

Cooperative distributions paid (3a) Market livestock

Agricultural program payments (4a) Accounts receivable

Crop insurance proceeds (6a) Unpaid cooperative distributions

Custom hire income (7) Breeding livestock

Other income (8), cash only Other current assets

Sales of breeding livestock Subtotal of income adjustments

Hedging accounts withdrawals b. Net income adjustment (ending − beginning)

a. Total Cash Income c. Gross Farm Revenue (a + b)

Expenses

Cash Expenses (numbers in ( ) refer to IRS Schedule F) Expense Adjustments (paid in advance) Beginning Ending

Car and truck expenses (10) Investment in growing crops

Chemicals (11) Commercial feed on hand

Conservation expenses (12) Prepaid expenses

Custom hire (13) Supplies on hand

Employee benefits (15) Subtotal of adjustments

Feed purchased (16) e. Net adjustment (beginning − ending)

Fertilizer and lime (17) Expense Adjustments (due) Beginning Ending

Freight, trucking (18) Farm accounts payable

Gasoline, fuel, oil (19) Farm taxes due

Insurance (20) Subtotal of adjustments (expenses due)

Interest paid (21a + 21b) f. Net adjustment (ending − beginning)

Labor hired (22) g. Depreciation (Schedule J + L + M)

Pension and profit-share plans (23) h. Total Operating Expenses (d + e + f + g)

Rent or lease payments (24a + 24b) (excluding interest)

Repairs, maintenance (25) i. Net Farm Income from Operations (c − h)

Seeds, plants (26) Interest Adjustments Beginning Ending

Storage, warehousing (27) Accrued interest

Supplies purchased (28) j. Net interest expense

Taxes (farm) (29) (cash − beginning + ending)

Utilities (30) Total Farm Expenses (h + j)

Vet. fees, medicine, breeding (31) k. Sales of farmland

Other expenses (32), cash only l. Cost value of land sold

Livestock purchased m. Capital gains or losses (k − l)

Hedging accounts deposits

d. Total Cash Expenses n. Net Farm Income (accrual) (i − j + m)

Net Farm Income (cash) (a − d)

Value of Farm Production

(c − purchases of feed & livestock)

Page 8

Your Farm Income Statement

Statement of Cash Flows

Name _______________________________________________________________ Year _______________________________

Cash In Cash Out

Cash farm income and expenses (operating)

Total cash income (line a, net farm income statement) xxx

Total cash expenses (line d, net farm income statement) xxx

Capital assets (investing)

Sales of capital assets xxx

Cost of purchases and trades xxx

Loans (financing)

New loans received xxx

Principal paid on loans xxx

Nonfarm (withdrawals)

Nonfarm income invested in the farm business xxx

Cash withdrawn from the farm for family living, taxes, savings, etc. xxx

Cash on hand (balance in farm checking and savings accounts, excluding hedging accounts)

Beginning of year xxx

End of year xxx

Total of cash in and cash out*

*If all cash transactions are included correctly, the totals for the two columns will be approximately equal.

Statement of Owner Equity

Name _______________________________________________________________ Year _______________________________

Cost Value Market Value

a. Farm net worth, beginning of year

(Line g, beginning net worth statement)

b. Change in market value of capital assets (net of depreciation) xxx

(Line i, ending net worth statement, market value _____________ minus cost value _____________)

c. Net farm income (accrual)

(Line n, net farm income statement)

same value for cost and market

d. Net nonfarm withdrawals: (nonfarm income invested − cash withdrawn)

(see statement of cash flows)

same value for cost and market

e. Calculated change in net worth (b + c + d)

f. Farm net worth, end of year (Line g, ending net worth statement)

g. Actual change in net worth (f − a)

(line e should approximately equal line g)

h. Percent of net farm income retained in the business this year ((c + d) / c) xxx

%

i. Percent of change in market value net worth from retained earnings this year

(g, cost value / g, market value)

xxx

%