UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT

2021

REVIEW

OF MARITIME

TRANSPORT

Geneva, 2021

REVIEW OF MARITIME TRANSPORT 2021

ii

© 2021, United Nations

All rights reserved worldwide

Requests to reproduce excerpts or to photocopy should be addressed to the Copyright Clearance Centre

at copyright.com.

All other queries on rights and licences, including subsidiary rights, should be addressed to:

United Nations Publications

405 East 42nd Street, New York, New York

10017 United States of America

Email: [email protected]

Website: https://shop.un.org

The designations employed and the presentation of material on any map in this work do not imply the

expression of any opinion whatsoever on the part of the United Nations concerning the legal status of

any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or

boundaries.

Mention of any rm or licensed process does not imply the endorsement of the United Nations.

This publication has been edited externally.

United Nations publication issued by the United Nations Conference on Trade and Development.

UNCTAD/RMT/2021

ISBN: 978-92-1-113026-3

eISBN: 978-92-1-000097-0

ISSN: 0566-7682

eISSN: 2225-3459

Sales No. E.21.II.D.21

REVIEW OF MARITIME TRANSPORT 2021

iii

Acknowledgements

The Review of Maritime Transport 2021 was prepared by UNCTAD under the overall guidance of Shamika

N. Sirimanne, Director of the Division on Technology and Logistics of UNCTAD, and under the coordination

of Jan Hoffmann, Head of the Trade Logistics Branch, Division on Technology and Logistics. Regina

Asariotis, Gonzalo Ayala, Mark Assaf, Celine Bacrot, Hassiba Benamara, Dominique Chantrel, Amélie

Cournoyer, Marco Fugazza, Poul Hansen, Jan Hoffmann, Tomasz Kulaga, Anila Premti, Luisa Rodríguez,

Benny Salo, Kamal Tahiri, Hidenobu Tokuda, Pamela Ugaz and Frida Youssef were contributing authors.

The report benetted from reviews and contributions by ofcials from the International Maritime

Organization, the International Labour Organization partners of the TrainForTrade Port Management

Programme and the ve regional commissions of the United Nations (ECA, ECE, ECLAC, ESCAP, and

ESCWA): Julian Abril Garcia, Peter Adams, Mario Apostolov, Yarob Badr, Jan de Boer, Aicha Cherif,

Ismael Cobos Delgado, Yann Duval, Martina Fontanet Solé, Fouad Ghorra, Fredrik Haag, Robert Lisinge,

Dorota Lost-Sieminska, Ricardo Sanchez, Lynn Tan, Lukasz Wyrowski and Brandt Wagner.

Comments and suggestions from the following reviewers are gratefully acknowledged: Hashim Abbas

Syed, Roar Adland, Stefanos Alexopoulos, Jason Angelopoulos, Tracy Chatman, Trevor Crowe, Neil

Davidson, Juan Manuel Díez Orejas, Mahin Faghfouri, Mike Garrat, Nadia Hasham, Joe Hiney, Julian

Hoffmann Anton, Onno Hoffmeister, Roel Janssens, Lars Jensen, Björn Klippel, Eleni Kontou, Juan

Manuel, Antonis Michail, Turloch Mooney, Richard Morton, Plamen Natzkoff, Jean-Paul Rodrigue, Peter

Sand, Torbjorn Rydbergh, Alastair Stevenson, Stelios Stratidakis, Christa Sys, Antonella Teodoro and

Ruosi Zhang. Experts from the International Chamber of Shipping reviewed chapter 2.

Comments received from UNCTAD divisions as part of the internal peer review process, as well as

comments from the Ofce of the Secretary-General, are acknowledged with appreciation.

The Review was edited by Peter Stalker. Administrative, editing, and proofreading support was provided

by Wendy Juan. Magali Studer designed the publication, and Juan Carlos Korol did the formatting.

Special thanks are also due to Vladislav Shuvalov for reviewing the publication in full.

REVIEW OF MARITIME TRANSPORT 2021

iv

TABLE OF CONTENTS

Acknowledgements .............................................................................................................................iii

Abbreviations

....................................................................................................................................... ix

Note

.....................................................................................................................................................xii

Overview

............................................................................................................................................xiv

1. International maritime trade and port trafc ..............................................1

A. Volumes of international maritime trade and port trafc ...................................................... 3

B. Outlook and longer-term trends ....................................................................................... 19

C. Policy considerations and action areas ............................................................................ 23

2. Maritime transport and infrastructure .......................................................29

A. The world eet ................................................................................................................ 31

B. Shipping companies and operations: adapting maritime transport supply

in an uncertain environment ............................................................................................ 42

C. Port services and infrastructure supply ............................................................................ 46

D. The Impact of COVID-19 on ports: lessons from the UNCTAD TrainForTrade Port

Management Programme ............................................................................................... 49

E. Summary and policy considerations ................................................................................ 54

3. Freight rates, maritime transport costs and their impact on prices ........57

A. Record-breaking container freight rates .......................................................................... 59

B. Dry bulk freight rates also reach highs ............................................................................. 64

C. Tanker freight rates dip to the lowest levels ever ............................................................. 65

D. Economic impact of high container freight rates, particularly in smaller countries ............. 66

E. Structural determinants of maritime transport costs ........................................................ 70

F. Summary and policy considerations ................................................................................ 74

Technical Notes ............................................................................................................... 78

4. Key performance indicators for ports and the shipping eet ..................87

A. Port calls and turnaround times ....................................................................................... 89

B. Liner shipping connectivity .............................................................................................. 93

C. Port cargo handling performance ................................................................................... 99

E. Greenhouse gas emissions by the world eet ................................................................ 105

F. Summary and policy considerations .............................................................................. 106

5. The COVID-19 seafarer crisis .................................................................. 109

A. Seafarers crisis – recent developments ......................................................................... 111

B. Seafarer crisis – implementation of the ILO Maritime Labour Convention, 2006,

as amended (MLC 2006)

............................................................................................... 115

C. Crew changes and key worker status – other relevant international legal instruments .... 117

D. The way forward ........................................................................................................... 119

6. Legal and regulatory developments and the facilitation

of maritime trade

....................................................................................125

A. Technological developments in the maritime industry .................................................... 127

B. Regulatory developments relating to international shipping, climate change

and other environmental issues

..................................................................................... 128

C. Legal and regulatory implications of the COVID-19 pandemic ....................................... 133

D. Other legal and regulatory developments affecting transportation .................................. 133

E. Maritime transport within the WTO Trade Facilitation Agreement .................................. 135

F. FAL Convention ............................................................................................................ 139

G. ASYCUDA ASYHUB case studies ................................................................................ 141

H. Summary and policy considerations .............................................................................. 142

REVIEW OF MARITIME TRANSPORT 2021

v

Tables

1 World eet by principal vessel type, 2020–2021 ................................................................... xvi

2 Five largest seafarer-supplying countries 2021 supplying countries 2021 ............................... xx

1.1 International maritime trade, 1970–2020 ..................................................................................3

1.2 International maritime trade 2019–2020, by type of cargo, country group and region ..............4

1.3 World economic growth, 2019–2021 .......................................................................................6

1.4 Growth in the volume of world merchandise trade, 2019–2021 ...............................................7

1.5 Tanker trade, 2019–2020.......................................................................................................11

1.6 Dry bulk trade 2019–2020 .....................................................................................................12

1.7 Major dry bulk and steel: producers, users, exporters, and importers, 2020 ..........................13

1.8 Containerized trade on East-West trade routes, 2016–2020 ..................................................15

1.9 Containerized trade on major East-West trade routes, 2014–2021 ........................................15

1.10 World container port throughput by region, 2019–2020 .........................................................17

1.11 International maritime trade developments forecasts, 2021–2026 ..........................................19

2.1 World eet by principal vessel type, 2020–2021 ....................................................................31

2.2 Age distribution of world merchant eet by vessel type, 2021

and average age 2020–2021

.................................................................................................32

2.3 Top 25 ship-owning economies, as of 1 January 2021 ..........................................................35

2.4 Ownership of the world eet, ranked by carrying capacity in dead-weight tons, 2021 ............36

2.5 Leading ags of registration by dead-weight tonnage, 2021 ..................................................38

2.6 Leading ags of registration, ranked by value of total tonnage, 2021 (million US dollars)

and principal vessel types

......................................................................................................39

2.7 Deliveries of newbuildings by major vessel types and countries of construction, 2020 ...........39

2.8 Reported tonnage sold for ship recycling by major vessel type

and country of ship recycling, 2020

.......................................................................................41

2.9 Status of uptake of selected technologies in global shipping, as of 14 June 2021 ..................42

2.10 Some proposed IMO measures to reduce greenhouse gas emissions ...................................43

2.11 World eet by fuel type as of 1 January 2021 .........................................................................45

2.12 Industrial port projects capitalizing on green opportunities to generate

new revenue streams.............................................................................................................48

2.13 Factors affecting the development of smart green ports ........................................................49

2.14 Port Performance Scorecard indicators, 2016–2020 .............................................................50

3.1 Contract freight rates, inter-regional, 2018–2020, $ per 40-foot container .............................62

4.1 Time in port, age, and vessel sizes, by vessel type, 2020, world total ....................................90

4.2 Port calls and median time spent in port, container ships, 2020, top 25 countries .................91

4.3 Top 25 ports under the World Bank IHS Markit Container Port Performance Index 2020 .......99

4.4 Minutes per container move, by range of call size, top 25 countries by port calls .................101

4.5 Cargo and vessel handling performance for dry bulk carriers. Top 30 economies

by vessel arrivals, average values for 2018 to rst half of 2021

.............................................103

4.6 Cargo and vessel handling performance for tankers. Top 30 countries

by vessel arrivals, average values for 2018 to rst half of 2021

.............................................104

5.1 Neptune Declaration Crew Change Indicator, July 2021 ......................................................113

5.2 Five largest seafarer-supply countries, 2021 ........................................................................115

6.1 Key performance indicators of the Kenya Trade Information Portal .......................................138

REVIEW OF MARITIME TRANSPORT 2021

vi

Figures

1 International maritime trade, world gross domestic product (GDP)

and maritime trade-to-GDP ratio, 2006 to 2021

.................................................................... xii

2 Simulated impact of current container freight rate surge on import

and consumer price levels

..................................................................................................... xv

3 Median time in port, number of port calls, and maximum vessel sizes,

by country, container ships, 2020

.........................................................................................xvii

1.1 International maritime trade, world gross domestic product (GDP)

and maritime trade-to-GDP ratio, 2006 to 2021

......................................................................5

1.2 Participation of developing countries in international maritime trade, selected years .................5

1.3 International maritime trade, by region, 2020 ...........................................................................5

1.4 International maritime trade by cargo type, selected years .......................................................8

1.5 International maritime trade in cargo ton-miles, 2001–2021 .....................................................9

1.6 World capesize dry bulk trade by exporting region in tons and ton-miles, 2019–2020 ............10

1.7 World ultra-large tanker trade by exporting region in ton and ton-miles , 2018–2020 .............10

1.8 Global containerized trade, 1996–2021 .................................................................................14

1.9 Global containerized trade by route, 2020 .............................................................................14

1.10 World container port throughput by region, 2019–2020 .........................................................18

1.11 Leading 20 global container ports, 2019–2020 ......................................................................18

2.1 Annual growth rate of world eet, dead-weight tonnage, 2000–2020 .....................................31

2.2 Age distribution of the global eet, share of the global carrying capacity, 2012–2021 .............33

2.3 Age distribution of the eet, as at beginning of 2021, per development status groups ...........33

2.4 Share of mega-vessels in the global container ship eet carrying capacity

by TEU, 2011–2021

..............................................................................................................34

2.5 Number of mega-containerships ............................................................................................34

2.6 Mega-vessel distinct journeys through the Panama and Suez canals,

daily averages, from 2012 until 4 June 2021

..........................................................................34

2.7 Live and on-order global eet by ship type .............................................................................37

2.8 Growth of world eet orderbook, 2012–2021, percentage change

in dead-weight tonnage

.........................................................................................................40

2.9 World tonnage on order, selected ship types, 2000–2021 .....................................................41

2.10 Percentage change in cost intensity by ship segment, average size

and median distance travelled

...............................................................................................44

2.11 Cargo and revenue, 2016–2020 ............................................................................................51

2.12 Average revenue mix of ports, 2016–2020 .............................................................................52

3.1 Growth of demand and supply in container shipping, 2007–2021, percentage ......................59

3.2 CCFI composite index, 2011-2021 (quarterly) ........................................................................60

3.3 Shanghai Containerized Freight Index weekly spot rates, 1 July 2011 to 30 July 2021,

selected routes

.....................................................................................................................60

3.4 New ConTex index, July 2011–July 2021 ...............................................................................63

3.5 Baltic Exchange Dry Index, January 2010–July 2021 .............................................................65

3.6 Average weighted earnings all bulkers ($/day), July 2001–July 2021 ......................................65

3.7 Average earnings, all tankers, July 2011–July 2021 ...............................................................66

3.8 Simulated impact of current container freight rate surge on import

and consumer price levels

.....................................................................................................67

REVIEW OF MARITIME TRANSPORT 2021

vii

3.9 Simulated impacts of the container freight rate surge on consumer price levels,

by country and by product.....................................................................................................68

3.10 Simulated impacts of container freight rate surges on prices for importers,

consumers and rms, global average

....................................................................................69

3.11 Simulated impact of container freight rate surges on production costs,

by country and size of economy

............................................................................................69

3.12 Simulated dynamic impacts of container freight rate increase on industrial production ...........70

3.13 Transport costs for importing goods by transport mode, world, LDCs,

and LLDCs, 2016, percentage of FOB value

..........................................................................71

3.14 Transport costs heatmap for importing goods, all modes of transport, 2016,

percentage of FOB value

.......................................................................................................71

3.15 Maritime transport costs for importing goods and distances from trading partners ................72

3.16 Maritime transport costs for importing goods, by country and size of economy .....................73

3.17 Impact of structural determinants on maritime transport costs for importing goods ...............73

3.18 Maritime transport costs by direction of the trade imbalance .................................................74

3.19 Impacts of trade imbalance and trade volume on maritime transport costs ............................74

4.1 Port calls per half year, world total, 2018–2020 ......................................................................89

4.2 Port calls per half year, regional totals, 2018–2020 ................................................................89

4.3 Container ship port calls and time in port, 2020 .....................................................................90

4.4 Container ship port calls and maximum ship sizes, 2020 .......................................................91

4.5 Container ship port calls in Africa and time in port, 2020 .......................................................92

4.6 Container ship port calls in Africa and maximum ship sizes, 2020 ..........................................92

4.7 Median time in port, number of port calls, and maximum vessel sizes, per country,

container ships, 2020

............................................................................................................92

4.8 Liner shipping connectivity index, top 10 countries, rst quarter 2006

to second quarter 2021

.........................................................................................................93

4.9 Port Liner Shipping Connectivity Index, top 10 ports as of second quarter 2021,

rst quarter 2006 to second quarter 2021

.............................................................................94

4.10 Liner Shipping Connectivity Index, country and port level, 2020 .............................................95

4.11 Trends in global container ship deployment, rst quarter 2006 to second quarter 2021 .........96

4.12 Trends in vessel sizes and number of companies providing services,

selected countries, rst quarter 2006 to second quarter 2021

...............................................97

4.13 Relationship between maximum vessel sizes, deployed capacity, and the number

of companies, second quarter 2021

......................................................................................98

4.14 Liner Shipping Bilateral Connectivity Index (LSBCI) and its components,

rst quarter 2006 to second quarter 2021

.............................................................................99

4.15 Minutes per container move for container ships, by range of port call size ...........................100

4.16 Time in port (hours) for container ships, by range of port call size ........................................100

4.17 Correlation between time in port (hours) and minutes per container move, all call sizes ........101

4.18 Correlation between time in port (hours) and minutes per container move,

only calls with 1001 to 1500 containers per call

...................................................................101

4.19 Carbon dioxide emissions by vessel type, monthly, million tons, 2011–2021 ........................105

4.20 Carbon dioxide emissions by ag state, annual, 2011–2020, million tons.............................106

REVIEW OF MARITIME TRANSPORT 2021

viii

Boxes

1 Implications of AfCFTA for maritime transport in Africa ...........................................................20

2.1 Divided views on whether oil should be replaced by LNG ......................................................46

2.2 Building port resilience UNCTAD experience ..........................................................................46

2.3 Guidance and standards for intermodal operations ................................................................47

2.4 Port performance analysis of the Port of Gijon in 2020 ...........................................................51

2.5 Port performance analysis of the national port system in Peru in 2020 ...................................52

2.6 Gender and development in the Philippine Ports Authority and its journey .............................53

3.1 Impact of COVID-19 on maritime freight rates in the Arab region ...........................................61

4.1 Port performance in Latin America and the Caribbean – differences between

types of terminals

................................................................................................................102

5.1 The case of the Philippines ..................................................................................................114

6.1 The Framework Agreement on Facilitation of Cross-Border Paperless Trade in Asia

and the Pacic - Maritime implications

.................................................................................138

6.2 IMO Compendium on Facilitation and Electronic Business ...................................................139

6.3 Components of the Digitizing Global Maritime Trade project ...............................................141

6.4 Customs formalities concerning entry or exit .......................................................................142

REVIEW OF MARITIME TRANSPORT 2021

ix

ABBREVIATIONS

AfCFTA African Continental Free Trade Area

AGTC European Agreement on Important International Combined Transport Lines

APEC Asia-Pacic Economic Cooperation

ASYCUDA Automated System for Customs Data

ASYHUB ASYCUDA data integration system

B2B business to business

B2G business to government

BIMCO Baltic and International Maritime Council

CAPEX capital expenditure

CCFI China Containerized Freight Index

CIF cost, insurance and freight

CII Carbon Intensity Indicator

CO

2

carbon dioxide

CPPI Container Port Performance Index

DGMT Digitizing Global Maritime Trade

dwt deadweight tonnage

EBITDA earnings before interest, taxes, depreciation and amortization

ECA Economic Commission for Africa

ECE United Nations Economic Commission for Europe

ECLAC United Nations Economic Commission for Latin America and the Caribbean

EEDI Energy Efciency Design Index

EEXI Energy Efciency Existing Ship Index

ESCAP United Nations Economic Commission for Asia and the Pacic

ESCWA United Nations Economic and Social Commission for Western Asia

eSW electronic single window

eTIR electronic International Road Transport system

EU European Union

FAL Convention Convention Facilitation of International Maritime Trafc

FIATA International Federation of Freight Forwarders Associations

FOB free on board

REVIEW OF MARITIME TRANSPORT 2021

x

G2B government to business

GAD gender and development

GDP Gross domestic product

GT Gigaton

GTCDIT Global Transport Costs Dataset for International Trade

GVC global value chain

HFO heavy fuel oil

ICAO International Civil Aviation Organization

ICS Institute Of Chartered Shipbrokers

IFO intermediate fuel oil

ILO International Labour Organization

IMF International Monetary Fund

IMO International Maritime Organisation

IOM International Organization for Migration

IOPC FUNDS International Oil Pollution Compensation Funds

IRU International Road Transport Union

ISM International Safety Management

ISO International Standards Organization

ISPS International Ship and Port Facility Security

ITF International Transport Workers' Federation

ITS intelligent transport systems

kw kilowatt

LDC least developed country

LLDC landlocked developing country

LNG liquied natural gas

LPG liquied petroleum gas

MARPOL

Convention

International Convention for the Prevention of Pollution from Ships

MASS maritime autonomous surface ship

MDH Maritime Declaration of Health

MDO marine diesel oil

MEPC IMO Marine Environment Protection Committee

MGO marine gasoil

REVIEW OF MARITIME TRANSPORT 2021

xi

MLC Maritime Labour Convention

MMT-RDM Multi-Modal Transport Reference Data Model

MNSW maritime national single window

MSC IMO Maritime Safety Committee

MSW maritime single window

NTFC National Trade Facilitation Committee

OECD Organisation for Economic Co-operation and Development

OPEC Organization of the Petroleum Exporting Countries

PCS port community system

PHEIC public health emergency of international concern

PIANC World Association for Waterborne Transport Infrastructure

PPA Philippine Ports Authority

PPPs public-private partnerships

PPS Port Performance Scorecard

R&D research and development

SCFI Shanghai Containerized Freight Index

SID Seafarers’ Identity Document

SIDS small island developing states

STCW Standards of Training, Certication and Watchkeeping for Seafarers

TEU twenty-foot-equivalent unit

TIP Trade Information Portal

UN/CEFACT The United Nations Centre for Trade Facilitation and Electronic Business

UNCITRAL United Nations Commission on International Trade Law

UNCTAD United Nations Conference on Trade and Development

UNDESA UN Department of Economic and Social Affairs

UNFCCC United Nations Framework Convention on Climate Change

UNOHRLLS

United Nations Ofce of the High Representative for the Least Developed

Countries, Landlocked Developing Countries and Small Island

Developing States

VLSFO very low sulphur fuel oil

WCO World Customs Organization

WHO World Health Organization

WIOD World Input-Output Database

WTO World Trade Organization

REVIEW OF MARITIME TRANSPORT 2021

xii

NOTE

The Review of Maritime Transport is a recurrent publication prepared by the UNCTAD secretariat

since 1968 with the aim of fostering the transparency of maritime markets and analysing relevant

developments. Any factual or editorial corrections that may prove necessary, based on comments made

by Governments, will be reected in a corrigendum to be issued subsequently.

This edition of the Review covers data and events from January 2020 until June 2021. Where possible,

every effort has been made to reect more recent developments.

All references to dollars ($) are to United States dollars, unless otherwise stated.

“Ton” means metric ton (1,000 kg) and “mile” means nautical mile, unless otherwise stated.

Because of rounding, details and percentages presented in tables do not necessarily add up to the

totals.

Two dots (..) in a statistical table indicate that data are not available or are not reported separately.

All websites were accessed in September 2021.

The terms “countries” and “economies” refer to countries, territories or areas.

Since 2014, the Review of Maritime Transport does not include printed statistical annexes. UNCTAD

maritime statistics are accessible via the following links:

All datasets: http://stats.unctad.org/maritime

Merchant eet by ag of registration: http://stats.unctad.org/eet

Share of the world merchant eet value by ag of registration: http://stats.unctad.org/vesselvalue_

registration

Merchant eet by country of ownership: http://stats.unctad.org/eetownership

Share of the world merchant eet value by country of benecial ownership: http://stats.unctad.org/

vesselvalue_ownership

Ship recycling by country: http://stats.unctad.org/shiprecycling

Shipbuilding by country in which built: http://stats.unctad.org/shipbuilding

Seafarer supply: http://stats.unctad.org/seafarersupply

Liner shipping connectivity index: http://stats.unctad.org/lsci

Liner shipping bilateral connectivity index: http://stats.unctad.org/lsbci

Container port throughput: http://stats.unctad.org/teu

Port liner shipping connectivity index: http://stats.unctad.org/plsci

Port call performance (Time spent in ports, vessel age and size), annual: http://stats.unctad.org/

portcalls_detail_a

Port call performance (Time spent in ports, vessel age & size), semi-annual: http://stats.unctad.org/

portcalls_detail_sa

Number of port calls, annual: http://stats.unctad.org/portcalls_number_a

Number of port calls, semi-annual: http://stats.unctad.org/portcalls_number_sa

Seaborne trade: http://stats.unctad.org/seabornetrade

National maritime country proles: http://unctadstat.unctad.org/CountryProle/en-GB/index.html

REVIEW OF MARITIME TRANSPORT 2021

xiii

Vessel groupings used in the Review of Maritime Transport

Group Constituent ship types

Oil tankers Oil tankers

Bulk carriers Bulk carriers, combination carriers

General cargo ships Multi-purpose and project vessels, roll-on roll-off cargo ships,

general cargo ships

Container ships Fully cellular container ships

Other ships Liqueed petroleum gas carriers, liqueed natural gas carriers,

parcel (chemical) tankers, specialized tankers, refrigerated container

ships, offshore supply vessels, tugboats, dredgers, cruise, ferries,

other non-cargo ships

Total all ships Includes all the above-mentioned vessel types

Approximate vessel-size groups according to commonly used shipping terminology

Crude oil tankers

Ultralarge crude carrier 320,000 dead-weight tons (dwt) and above

Very large crude carrier 200,000–319,999 dwt

Suezmax crude tanker 125,000–199,999 dwt

Aframax/longe-range 2

crude tanker 85,000–124,999 dwt

Panamax/long-range 1

crude tanker 55,000–84,999 dwt

Medium-range tankers 40,000–54,999 dwt

Short-range/Handy

tankers 25,000–39,000 dwt

Dry bulk and ore carriers

Capesize bulk carrier 100,000 dwt and above

Panamax bulk carrier 65,000–99,999 dwt

Handymax bulk carrier 40,000–64,999 dwt

Handysize bulk carrier 10,000–39,999 dwt

Container ships

Neo-Panamax Container ships that can transit the expanded locks of the Panama

Canal with up to a maximum 49 m beam and 366 m length overall;

eets with a capacity of 12,000–14,999 20-foot equivalent units (TEUs)

include some ships that are too large to transit the expanded locks of

the Panama Canal based on current dimension restrictions.

Panamax Container ships above 3,000 TEUs with a beam below 33.2 m, i.e., the

largest size vessels that can transit the old locks of the Panama Canal.

Post Panamax Fleets with a capacity greater than 15,000 TEUs include some ships

that are able to transit the expanded locks.

Source: Clarksons Research.

Note: Unless otherwise indicated, the ships mentioned in the Review of Maritime Transport include all propelled seagoing

merchant vessels of 100 gross tons and above, excluding inland waterway vessels, shing vessels, military vessels, yachts,

and xed and mobile offshore platforms and barges (with the exception of oating production storage, ofoading units and

drillships).

REVIEW OF MARITIME TRANSPORT 2021

xiv

Maritime transport navigated through the pandemic, but there was an

unprecedented humanitarian crisis for seafarers

While carriers generally managed to mitigate the shock and disruption, port and landside operations

found it more difcult to adjust, and seafarers were in a precarious situation as the pandemic triggered

an unprecedented global crew-change crisis. The health risks and related travel restrictions meant that

hundreds of thousands of seafarers could not return home, while an equivalent number were unable to

join their ships and to provide for their families.

OVERVIEW

Maritime transport deed the COVID-19 disruption. In 2020, volumes fell less

dramatically than expected and by the end of the year had rebounded, laying

the foundations for a transformation in global supply chains and new maritime

trade patterns

The COVID-19 pandemic disrupted maritime transport, though the outcome was less damaging than

initially feared. The shock in the rst half of 2020 caused maritime trade to contract by 3.8 per cent in the

year 2020. But in the second half of the year there was a nascent, if asymmetric, recovery, and by the third

quarter, volumes had returned, for both containerized trade and dry bulk commodities. However, there

has yet to be a full recovery for tanker shipping.

Maritime trade has performed better than expected partly because the COVID-19 pandemic unfolded in

phases and at different speeds, with diverging paths across regions and markets. The rebound in trade

ows was also the result of large stimulus packages, and increased consumer spending on goods, with

a growth in e-commerce, especially in the United States. Later, there was more general optimism in

advanced regions from the rollout of vaccines. But it was also partly due to unlocking pent-up demand for

cars, for example, and to restocking and inventory-building. The rebound was fairly swift because, unlike

the global nancial crisis of 2009, the downturn was not synchronized across the world.

In 2021, in tandem with the recovery in merchandise trade and world output, maritime trade is projected

to increase by 4.3 per cent (gure 1).The medium-term outlook also remains positive, though subject to

mounting risks and uncertainties, and moderated in line with projected lower growth in the world economy.

Over the past two decades, compound annual growth in maritime trade has been 2.9 per cent, but over

the period 2022–2026, UNCTAD expects that rate to slow to 2.4 per cent.

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

20122006 2007 2008 2009 2010 2011 2013 2014 2015 2016 2017 2018 2019 2020 2021

GDP Maritime trade Maritime trade-to-GDP ratio Average ratio

Average ratio 2006-2014

Average ratio 2015-2021

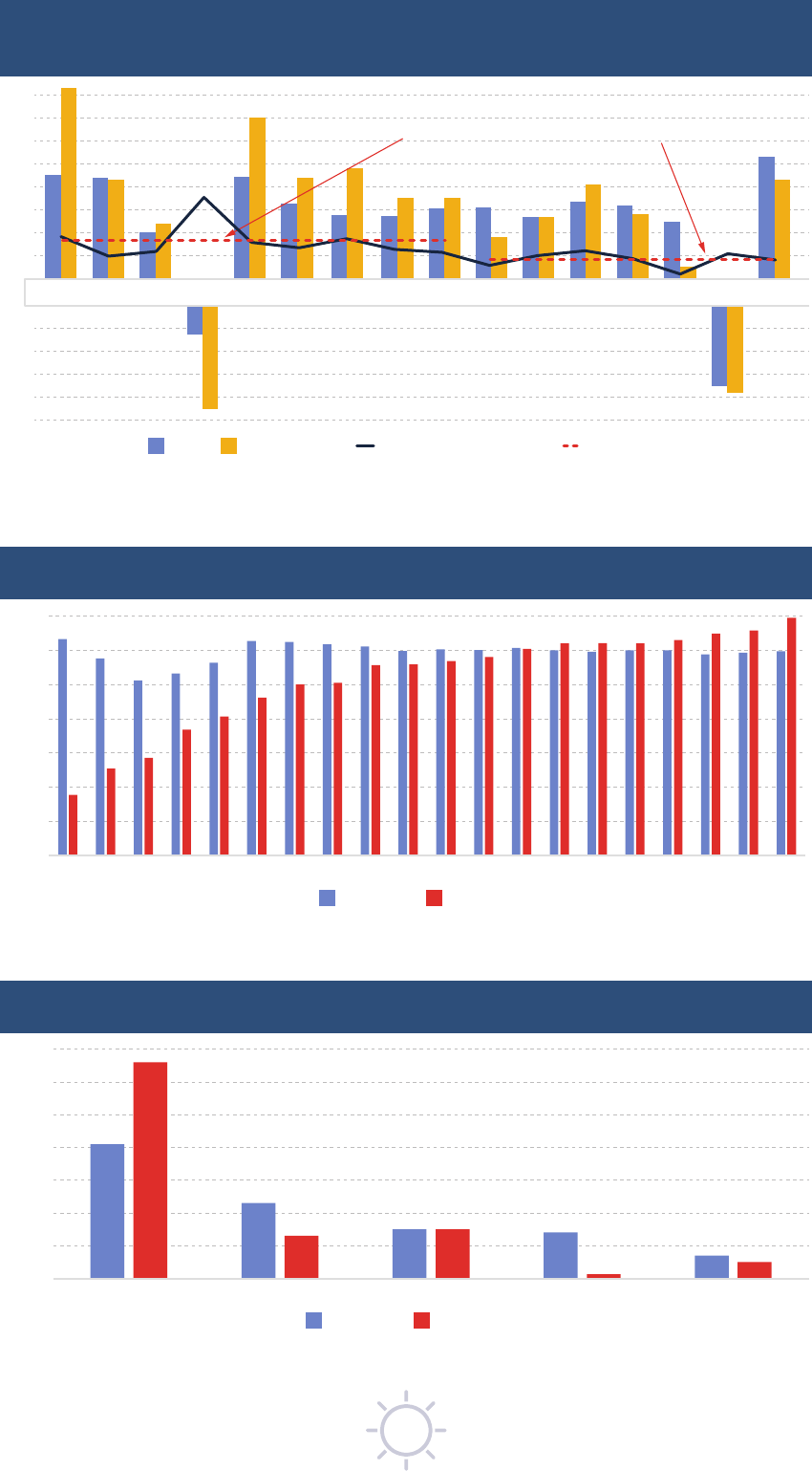

Figure 1 International maritime trade, world gross domestic product (GDP)

and maritime trade-to-GDP ratio, 2006 to 2021

(percentage annual change and ratio)

Source: UNCTAD calculations, based on the Review of Maritime Transport, various issues, data from UNCTADstat and

table 1.1 of the UNCTAD Trade and Development Report 2021. From recovery to resilience: The development dimension.

REVIEW OF MARITIME TRANSPORT 2021

xv

Hardest hit has been tanker shipping, but the impact has been less for

containerized trade, gas shipments, and dry bulk commodities

Lockdowns, travel restrictions and production cuts have compressed the demand for fuel. In 2020,

shipments of crude oil, rened petroleum products, and gas together fell by 7.7 per cent. The impact

was less, however, for dry bulk commodity trade: supported by strong demand from China for iron ore

and grain, total dry bulk trade fell by only 1.5 per cent. Containerized trade also resisted, falling by only

1.1 per cent. Global container port throughput fell at a roughly similar rate – and in 2020 totalled 815.6

million twenty-foot equivalent units (TEU).

Logistical bottlenecks, and soaring costs, along with an asymmetric

recovery, have heightened uncertainty

Maritime trade weathered the storm in 2020 and the short-term outlook remains positive. However, the

emerging multi-paced recovery is inherently fragile as many countries and regions continue to lag. In

addition to new pandemic risks and the dangers of a two-track vaccination pattern where developing

countries continue to fall behind, other risks are casting a shadow on the recovery. While not all countries

have been able to deploy large stimuli packages and support measures, an untimely ending of the existing

support measures in advanced economies could potentially stie growth and hinder the nascent recovery.

The pandemic’s impacts and legacies are likely to linger and the future shape and contours of the next

normal for the world economy remain uncertain.

The nascent recovery has also been hindered by supply-chain bottlenecks. The rebound in trade,

combined with pandemic-induced restrictions in logistics operations has led to shortages in equipment

and containers, along with less reliable services, congested ports and longer delays and dwell times.

For shipping, on the other hand, soaring freight rates, surcharges and fees have bolstered protability.

Freight rates increased further following the March 2021 closure of the Suez Canal. The grounding of

the 20,150-TEU container ship Ever Given blocked the canal, delaying ships heading for Europe, and

increasing the constraints on ship and port capacity. Some voyages had to be re-routed around the Cape,

adding up to 7,000 miles to the distance.

Whether the recovery lasts will depend critically on the path of the pandemic. Fresh waves of infection,

combined with low vaccination rates, especially in developing countries, have led to new lockdowns

and border closures. A broad-based recovery hinges to a large extent on a worldwide vaccine rollout.

The International Monetary Fund estimates that $50 billion are required to end the pandemic and roll out

vaccines across developing countries. This would bring not just health but also economic benets since

it would be tantamount to a large scale economic stimulus package that could accelerate economic

recovery and by 2025 generate some $9 trillion in additional global output.

Seafarers are increasingly being recognized as “key workers” who are keeping shipping and trade moving,

while also being at the front line of the health crisis. Since seafarers come predominantly from developing

regions, industry and government should move quickly to implement vaccine procurement and distribution

plans.

The longer-term outlook is being reshaped by structural megatrends

that transcend the pandemic and its immediate impact

Eventually, the logistical hurdles caused by large swings in demand could dissipate as global trade

patterns normalize. However, the pandemic has also accelerated megatrends that in the longer-term

could transform the maritime transport landscape.

By exposing the vulnerabilities of existing supply chains, the COVID-19 disruption has sharpened the need

to build resilience. COVID-19 emphasized the importance of ensuring continuity in supply chains and the

need for them to become more resilient, responsive, and agile.

Discussions over the future of globalization have ushered calls to take a fresher look at the conguration of

the extended supply chains to reduce heavy reliance on distant suppliers. Some are arguing that reshoring

and nearshoring will accelerate, resulting in deep reconguration of supply chains. While the structural

trends that had emerged over a decade ago and accelerated during recent trade tensions are likely to

result in changes to globalization patterns and features, an outright end to globalization per se is unlikely.

It may be fairly straightforward to reshore labour-intensive and low-value production, but it is more complex

to move production and switch suppliers for mid-and high-value-added manufacturing. Instead, enterprises

are likely to blend local and global sourcing, modifying their strategies according to product and geography

REVIEW OF MARITIME TRANSPORT 2021

xvi

– with a blend of reshoring, diversication, replication, and regionalization. Nevertheless, for the near future

China is likely to remain a leading manufacturing site. Automation could make reshoring and nearshoring

more economically viable in the longer term. Hybrid operating models involving just-in-time (i.e., material

moved just before its use in the manufacturing process) and just-in-case (i.e., where companies keep

large inventories to minimize stocks being sold out) supply chain models are likely to emerge. Combined,

these trends will change distances and routes, increasing the need for more exible shipping services.

They also entail implications for vessel types and sizes, ports of call, and distance travelled.

The pandemic has accelerated pre-existing digitalisation and environmental sustainability trends.

Technological advances have enabled shipping and ports to continue operations while minimizing

interaction and physical contact. New technologies have also stimulated the rise of online commerce

which has transformed consumer shopping habits and spending patterns. The growth in online trade

has increased the demand for distribution facilities and warehousing that are digitally enabled and offer

value-added services. All these developments are expected to generate new business opportunities for

shipping and ports as well as for other players in the maritime supply chain.

Technology will also be critical for advancing environmental sustainability. While designing their stimulus

packages and post-pandemic plans, many governments aim to harness the synergies between technology,

environmental protection, efciency, and resilience. Businesses and governments recognize that adapting

to the post-pandemic world and building back better requires adding economic, social and environmental

value and creating new business opportunities, not least for maritime transport.

Supply not keeping pace with demand

In 2020, the global commercial shipping eet grew by 3 per cent, reaching 99,800 ships

of 100 gross tons and above. By January 2021, capacity was equivalent to 2,13 billion

dead weight tons (dwt) (table 1). During 2020, delivery of ships declined by 12 per cent,

partly due to lockdown-induced labour shortages that disrupted marine-industrial activity.

The ships delivered were mostly bulk carriers, followed by oil tankers and container ships. As owners and

operators tried to cope with tight vessel supply, they were also buying more second-hand ships with a

resulting increase in prices. Recycling rates also increased in 2020, although compared to previous years,

the levels remain low.

During 2020, orders for new ships had declined by 16 per cent, continuing a downward trend observed in

previous years. In early 2021, however, shipping companies reacted to the capacity constraints with a surge

of new orders, especially for container ships for which orders were the highest for the last two decades.

There were also more orders for LNG carriers.

Table 1 World eet by principal vessel type, 2020–2021

(thousand dead-weight tons and percentage)

Principal types 2020 2021 Percentage change

2021 over 2020

Bulk carriers 879 725

42.47%

913 032

42.77% 3.79%

Oil tankers 601 342

29.03%

619 148

29.00% 2.96%

Container ships 274 973

13.27%

281 784

13.20% 2.48%

Other types of ships: 238 705

11.52%

243 922

11.43% 2.19%

Offshore supply 84 049

4.06%

84 094

3.94% 0.05%

Gas carriers 73 685

3.56%

77 455

3.63% 5.12%

Chemical tankers 47 480

2.29%

48 858

2.29% 2.90%

Other/not available 25 500

1.23%

25 407

1.19% -0.36%

Ferries and passenger ships 7 992

0.39%

8 109

0.38% 1.46%

General cargo ships 76 893

3.71%

76 754

3.60% -0.18%

World total 2 071 638 2 134 640 3.04%

Source: UNCTAD calculations, based on data from Clarksons Research.

Note: Propelled seagoing merchant vessels of 100 tons and above; beginning-of-year gures.

REVIEW OF MARITIME TRANSPORT 2021

xvii

0

5

10

15

20

25

30

8.7

LDC

3.2

LLDC

24.2

SIDS

10.6

World

(%)

0

1

2

3

4

5

6

7

8

2.2

LDC

0.6

LLDC

7.5

SIDS

1.5

World

(%)

Import price increases Consumer price increases

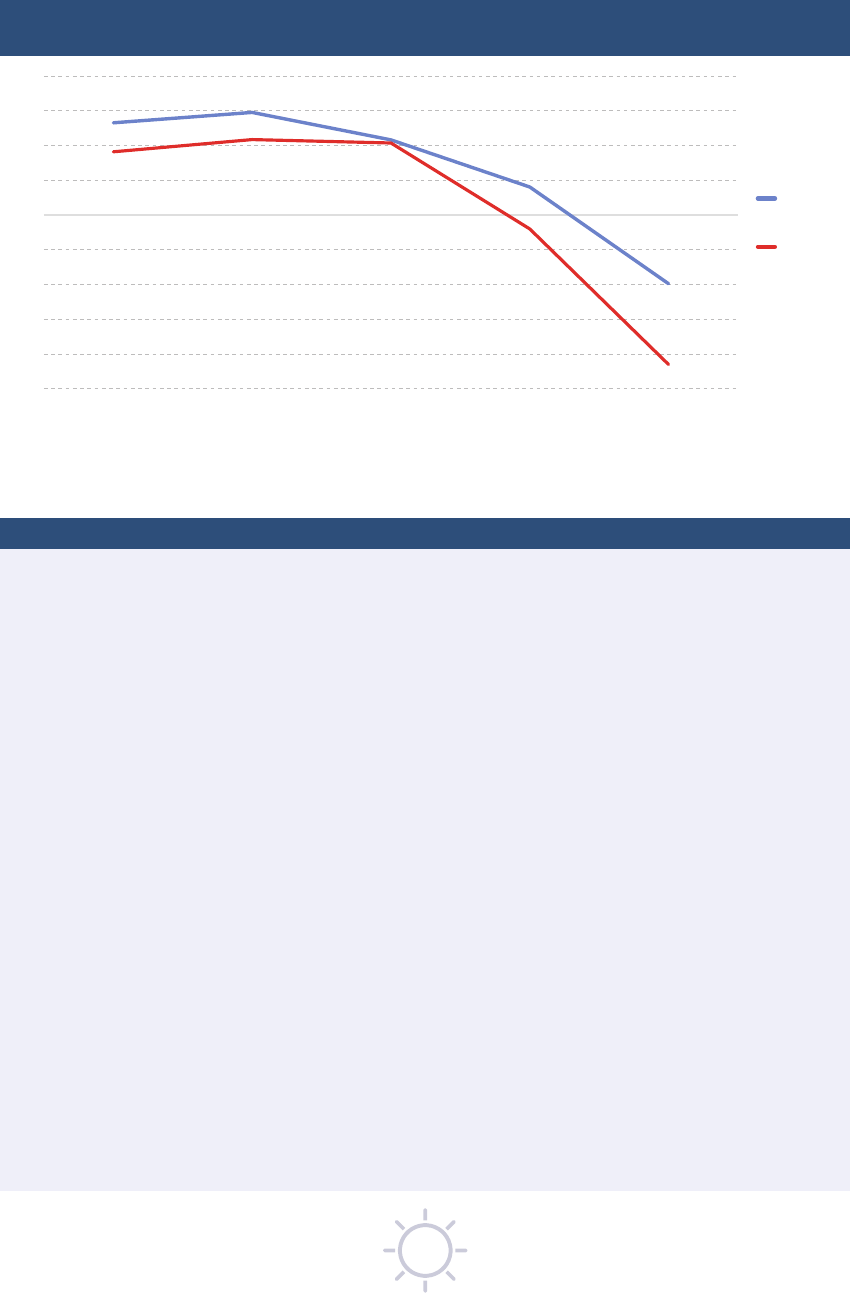

Figure 2 Simulated impact of current container freight rate surge on import and consumer

price levels

Sources: Based on data provided by Clarksons Research, Shipping Intelligence Network, the International Monetary Fund,

International Financial Statistics and Direction of Trade Statistics, UNCTADstat, and the World Bank, World Integrated Trade

Solution and Commodity Price Data (The Pink Sheet).

Note: The impact of container freight rate surges on prices is assessed based on a 243 per cent increase in the China

Containerized Freight Composite Index between August 2020 and August 2021. The simulation model assumes that freight

rates in August 2021 will be sustained over the remaining simulation period (September 2021 to December 2023) and all other

factors are held constant over the entire simulation period (August 2020 to December 2023).

During the second half of 2020, and into 2021, world trade gradually recovered but supply was less

elastic and constrained by COVID-19 related delays and congestion – leading to a signicant increase in

container freight rates.

The future demand/supply balance will also be impacted by regulatory requirements to align shipping

operations with decarbonization targets. Introduced under the auspices of the International Maritime

Organization (IMO), these new regulations will require replacing some of the existing eet so will entail

signicant costs. As well as creating a degree of uncertainty, this could reduce the capital available to

expand the eet to cater for trade growth.

Cost pressure and soaring rates and surcharges would weigh on smaller

players and prices

Since the second half of 2020 there has been an increase in freight rates. While demand for containerized

goods has been higher than expected, shipping capacity has been constrained by logistical hurdles and

bottlenecks and shortages in container shipping equipment. Unreliable schedules, and port congestion

have also led to a surge in surcharges and fees, including demurrage and detention fees.

These soaring costs are a challenge for all traders and supply chain managers, but especially for smaller

shippers who, compared with the larger players, may be less able to absorb the additional expense and

are at a disadvantage when negotiating rates and booking space on ships. Smaller shippers and low-value

paying cargo may thus nd it difcult to secure service contracts and could see their margins eroded.

Freight rates are expected to remain high. Demand is strong and there is growing uncertainty on the supply

side, with concerns about the efciency of transport systems and port operations. In the face of these cost

pressures and lasting market disruption, it is increasingly important to monitor market behaviour and ensure

transparency when it comes to setting rates, fees, and surcharges. There have been calls for governments to

intervene, and for regulators to apply closer oversight and address unfair market practices.

If sustained, the current surge in container freight rates, will signicantly increase both import and consumer

prices. UNCTAD’s simulation model suggests that global import price levels will increase on average by

11 percent as a result of the freight rate increases (gure 2). Hardest hit will be the small island developing

states (SIDS) who depend for their merchandise imports primarily on maritime transport and who are simulated

to face a cumulative increase of 24 per cent with a time lag of about a year.

Higher container freight rates will also have a sizeable impact on consumer prices. If container freight

rates remain at their current high levels, then in 2023 global consumer prices are projected to be 1.5 per

cent higher than they would have been without the freight rate surge. The impact is expected to be more

signicant for smaller economies that depend heavily on imported goods for much of their consumption

needs. In SIDS, the cumulative increase in consumer prices is expected to be 7.5 per cent and in the

Least Developed Countries (LDCs) 2.2 per cent.

REVIEW OF MARITIME TRANSPORT 2021

xviii

Some goods will be affected more than others by the surge in container freight rates. Most exposed are

goods manufactured through integrated supply chains. Globalized production processes entail a greater

use of shipping, with intermediate goods often crossing borders multiple times within and between

regions. This is the case, for example, for East Asian goods destined for major markets in North America

and Europe. For computers, and electronic and optical products, for example, the consumer price uplift

induced by the current freight rate surge could be 11 per cent.

Higher shipping costs will also affect some low-value-added products: for furniture, for example, and

textiles, garments and leather products, the consumer price uplifts could be ten per cent. These increases

could erode the competitive advantages of smaller economies that produce many of these goods. At the

same time, these countries will nd it more difcult to import the high-technology machinery and industrial

materials they need to move up the value chain, diversify their economies and achieve the Sustainable

Development Goals (SDGs).

Even in major economies, lingering high container freight rates and disruption in maritime transport in the

short- to medium-term threaten to undermine recovery. UNCTAD’s analysis concludes that in the United

States and the euro area, for example, a 10 per cent increase in container freight rates could lead to a

cumulative contraction in industrial production of around 1 per cent.

Structural factors keep maritime transport costs higher in developing

regions

The current historical highs in freight rates are largely driven by pandemic-induced shocks and unexpected

upward swings in shipping demand. But in the longer term, shipping and port prices are driven by structural

factors such as port infrastructure, economies of scale, trade imbalances, trade facilitation, and shipping

connectivity – all of which have lasting impacts on maritime transport costs and trade competitiveness. An

analysis based on a new UNCTAD-World Bank transport costs dataset, shows that signicant structural

improvements could reduce maritime transport costs by around four per cent. Interventions and policies

that address the structural determinants of maritime transport costs can thus help mitigate the impacts

from cyclical factors and disruptions.

Other structural issues that will increase prices include the new regulations on decarbonizing shipping.

The recently adopted IMO short-term measure on greenhouse gas reduction is expected to reduce

average shipping speeds and increase maritime transport costs, especially for developing countries, and

in particular the SIDS.

COVID-19 slows operations for ships and ports

In the rst half of 2020, reecting the slump in shipping demand, cargo-carrying ships made fewer port

calls. The number of calls subsequently increased, particularly in Europe, East Asia, and South-Eastern

Asia, albeit not yet to pre-pandemic levels.

In 2020, terminal operators, authorities, and intermodal transport providers took measures to contain

COVID-19 and, as a result, ships had to spend more time in ports that were operating more slowly. The

greatest delays were for dry break bulk carriers for which cargo operations tend to be less automated and

more labour-intensive so were slowed by measures to reduce social contact.

Turnaround times can differ signicantly between countries (gure 3). One group of countries with faster

turnarounds comprises those with fewer arrivals and only small ships and with only few containers loaded

and unloaded during each port call. These include Dominica, Saint Kitts and Nevis, and Saint Vincent

and the Grenadines. Another group with fast turnarounds comprises those that have the latest port

technologies and infrastructure and can accommodate the largest container vessels; they benet from

economies of scale and thus tend to attract the highest number of port calls. These include Japan, Hong

Kong China, and Taiwan Province of China. Efcient ports initiate a positive feed-back loop: high efciency

makes their ports attractive as ports of call, further boosting the number of arrivals. Countries in the middle

of the distribution report a wide range of median port waiting times, reecting differences in efciency and

other variables such as vessel age and cargo throughput.

Shipping and port performance is generally lower in developing countries. They have higher transport

costs and lower connectivity because they are often further away from their overseas markets and are

hampered by diseconomies of scale and lower levels of digitalization.

REVIEW OF MARITIME TRANSPORT 2021

xix

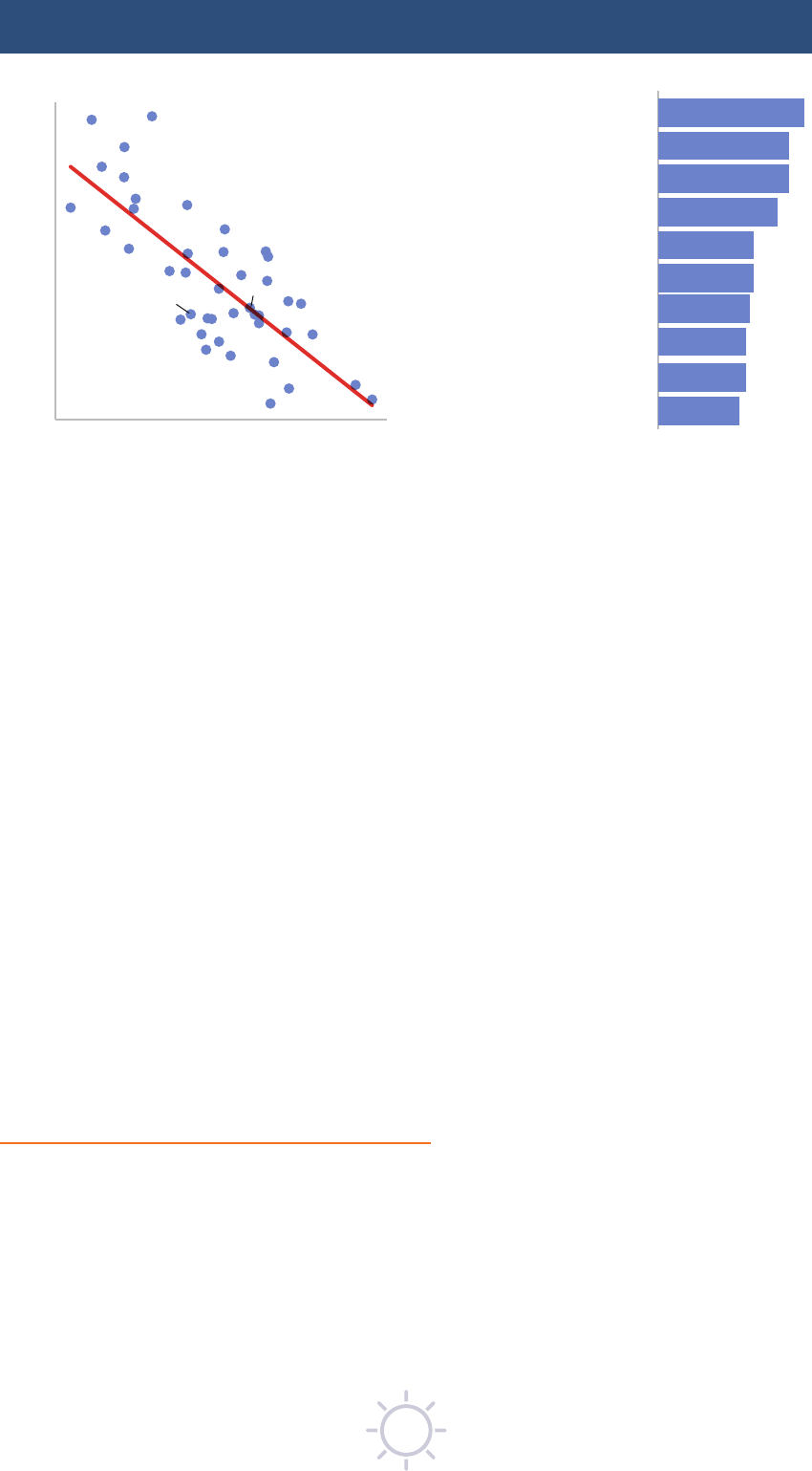

Figure 3 Median time in port, number of port calls, and maximum vessel sizes, by country,

container ships, 2020

0.50 day

1 day

2 days

4 days

8 days

100 1 000 10 000 100 000

Port calls

Median time in port

Maximum vessel

size (TEU)

1 000

5 000

10 000

15 000

20 000

Source: UNCTAD, based on data provided by MarineTrafc. Both axes in logarithmic scale.

Note: Ships of 1,000 GT and above. For the complete table of countries, see http://stats.unctad.org/maritime.

Positive trends in port governance and gender participation

Each year, UNCTAD uses data from its TrainForTrade Port Management Programme to benchmark

countries against each other using the Port Performance Scorecard (PPS). Many other port performance

projects focus on service provision such as cargo handling, but the PPS, which uses data for 26 indicators,

enables comparisons between entire port entities, providing data that is valuable for strategic planning

within ports and for evidence-based policy analysis at regional and state levels.

Member ports’ annual throughput in 2020 ranged from 1.5 million to 80.9 million tonnes. Around half of

were in the smallest category, less than 5 million tonnes, and the medium category, 5 million to 10 million

tonnes, a range of volumes that was similar across all regions.

Since 2015, one of the six main categories in the PPS scorecard has been the rate of female participation

in the port workforce. In 2019 and 2020, this remained low, at around 18 per cent. The rate was

signicantly higher in Europe at 25 per cent, though even here roles are not equally distributed between

men and women. Women tend to be better represented in management and administrative roles, for

which between 2019 and 2020 the proportion of women increased from 38 to 42 per cent. In this case,

Asian members were above average at 52 per cent compared with those in Europe at 39 per cent.

Women are far less likely to be working in cargo handling port operations. These results highlight the need

for strategic policy interventions to deliver on Sustainable Development Goal 5 to “Achieve gender equality

and empower all women and girls.”

Port and shipping performance depend on trade and transport

facilitation

Efcient maritime transport depends on effective trade and transport facilitation that reduces the time and

cost of customs and other trade procedures and integrate new technologies for administrative formalities.

Boosts the performance of the entire supply chain with positive effects on maritime transport.

The need for cross-border trade facilitation was highlighted by the COVID-19 pandemic, particularly for

trade in medical equipment, drugs and emergency goods such as vaccines and personal protection

equipment (PPE) – which could be held up at ports by red tape or by slow clearance procedures to

comply with regulatory requirements.

In recent years, the introduction of new technology in administrative processes has boosted efciency

along the logistics supply chain. This has involved digitalization and automation of customs processes,

REVIEW OF MARITIME TRANSPORT 2021

xx

paperless formalities, and the introduction of single-window services – the impetus for which was boosted

during the COVID-19 pandemic.

An example of the use of ICT, is UNCTAD’s Automated System for Customs Data (ASYCUDA) which

involves automation and digitalization in supply chains. A recent development, the ASYHUB solution,

smooths data transfer between ports of departure and arrival – using risk management concepts to help

speed up clearance procedures and avoid goods being stuck in ports unnecessarily.

Another ICT innovation based on UNCTAD technology is the Trade Information Portal (TIP) – a website

in each country that provides traders with easy access to information about trade regulations and

procedures. The UNCTAD TIP offers importers and exporters online, step-by-step guides to trade-related

procedures and also helps the country full its obligations arising from the World Trade Organization Trade

Facilitation Agreement. Today, 29 TIPs, based on UNCTAD technology, are being implemented globally

by UNCTAD and the International Trade Centre. Results have been very positive. TIPs are most advanced

in East Africa, where in Kenya, for example, greater transparency and simplication of a total of 52 trade

procedures so far have reduced the time spent waiting in the queue, at the counter and in between steps

by 110 hours, and the administrative fees for these 52 procedures by $482, i.e., about $11 per trade

procedure on average.

Digitalization allows a paperless environment whereby trade procedures are all carried out online. For the

traders this reduces time and cost and increases transparency and market access, while also reducing

physical contact and the risks of contagion. In addition, smart digital solutions improve public administration

of trade and boost efciency in export, import and transit operations. Moreover, by minimizing the use of

paper, trade facilitation can also help mitigate climate change.

Reforms in trade facilitation have been promoted by the multilateral trading system, particularly through

the WTO Facilitation Agreement and the IMO Convention on Facilitation of International Maritime Trafc.

These agreements provide common standards and regulations that have proved especially valuable

during the COVID-19 pandemic. By providing governments with guidance and incentives for reforming

trade facilitation, they have paved the way for further digitalization and enhanced transparency, and

for rationalizing administrative formalities. These developments also promote robust public-private

partnerships (PPPs), such as the National Trade Facilitation Committees and Port Community Systems

that involve the business community in port operations. Efcient maritime trade and transport will depend

on aligning and streamlining the mandates and work of the various PPPs.

A continuing crisis for seafarers stranded at sea

Globally there around 1.9 million seafarers working to facilitate the way we live. The BIMCO/ICS Seafarer

Workforce Report 2021 estimated the global supply of seafarers at 1,892,720, up from 1,647,494 in 2015. Of

these, 857,540 were ofcers, and 1,035,180 were ratings – the skilled seafarers who carry out support work.

The ve largest seafarer-supplying countries were the Philippines, the Russian Federation, Indonesia, China,

and India, representing 44 per cent of the global workforce (table 2).

Table 2 Five largest seafarer-supplying countries 2021 supplying countries 2021

All Seafarers Ofcers Ratings

1 Philippines Philippines Philippines

2 Russian Federation Russian Federation Russian Federation

3 Indonesia China Indonesia

4 China India China

5 India Indonesia India

Source: ISF and BIMCO, Seafarer Workforce Report 2021, London, 2021.

For the supplying countries seafarers are important sources of income. In 2019, the Philippines, for

example, earned $30.1 billion from its overseas workers – 9.3 per cent of GDP and 7.3 per cent of gross

national income (GNI) – of which $6.5 billion came from its seafarers. In 2020 total remittances fell 0.8 per

cent to $29.9 billion, with those from seafarers falling 2.8 per cent to $6.4 billion.

During the COVID-19 pandemic, seafarers continued to demonstrate great professionalism and dedication,

supporting the delivery of food, medical supplies, fuel, and other essential goods, and helping keep supply

chains active and global commerce running.

REVIEW OF MARITIME TRANSPORT 2021

xxi

However, hundreds of thousands of seafarers remain stranded at sea. Each month, crews need to be

changed over – to prevent fatigue and comply with international maritime regulations for safety, health

and welfare. Responding to COVID-19, governments closed many borders and imposed lockdowns and

prohibited people from disembarking thus temporarily suspending crew changes. As a consequence,

large numbers of seafarers have been unable to be replaced or repatriated after long tours of duty and had

to extend their service on board. Even over a year into the pandemic, due to these restrictions, and the

shortage of international ights, according to latest estimates by the International Chamber of Shipping,

around 250,000 seafarers remain stranded, far beyond the expiration of their contracts. Yet, there is still

no global consensus on uniform measures to allow for efcient crew changes and transfer.

During the pandemic, stakeholders, including international bodies, governments, and industry, have

issued recommendations and guidance – aiming to ensure that seafarers are healthy and protected

from COVID-19, have access to medical care, and are recognized as key workers and are vaccinated

as a matter of priority, and also that ships and port facilities meet international sanitary requirements.

Nevertheless, as the pandemic continues for a second year, seafarers remain very vulnerable.

With some notable exceptions, only a small proportion of the world’s seafarers have been vaccinated.

Belgium has demonstrated best practice, and July 2021 started a vaccination campaign for all seafarers

arriving in a Belgian port, regardless of nationality.

To address seafarers’ issues there has been a continuous level of cooperation among international

organizations and industry bodies, including IMO, ILO, WHO, UNCTAD, ICS, and ITF, which have repeatedly

expressed concern about the humanitarian crisis in the maritime shipping sector and urged Member

States to designate seafarers and other marine personnel as key workers, accept seafarers’ identity

documents as evidence of their key worker status, and allow exibility for ship owners and managers to

divert ships to ports where crew change is possible without imposing penalties.

On 1 December 2020, the UN General Assembly unanimously adopted a resolution: International

cooperation to address challenges faced by seafarers as a result of the COVID-19 pandemic to support

global supply chains (A/RES/75/17). This urges Member States to designate seafarers and other

marine personnel as key workers and encourages governments and other stakeholders to implement

the “Industry Recommended Framework of Protocols for ensuring safe ship crew changes and travel

during the Coronavirus (COVID-19) pandemic”. It also calls upon governments to facilitate maritime crew

changes – for example, by enabling them to embark and disembark, expediting travel and repatriation

efforts, and ensuring access to medical care. The resolution also requests IMO, ILO and UNCTAD to

inform the General Assembly at its 76

th

session on issues related to the resolution.

This follows earlier resolutions from other bodies. On 21 September 2020 the IMO’s Maritime Safety

Committee recommended action to facilitate ship crew change, access to medical care, and seafarer

travel during the COVID-19 pandemic. According to IMO, as of the end of June 2021, 60 Member

States and two Associate Members had signed on to designate seafarers as key workers. Similarly, on

8 December 2020 the Governing Body of the ILO, adopted the “Resolution concerning maritime labour

issues and the COVID-19 pandemic”.

In January 2021, the shipping industry issued the Neptune Declaration on Seafarer Wellbeing and Crew

Change, which by June 2021 had been signed by more than 600 companies and organizations. They

have also produced a Neptune Declaration Crew Change indicator which aggregates data from 10

leading ship managers which collectively have about 90,000 seafarers currently on board. This reported

that between June and July 2021 the situation appeared to be worsening, with more seafarers on

vessels beyond the expiry of their contract and more who had been on board for over 11 months – the

maximum length of time envisaged in the 2006 Maritime Labour Convention (MLC). Since the launch of

the indicator in May 2021, the proportion of seafarers on vessels beyond the expiry of their contract had

risen from 5.8 to 8.8 per cent while the proportion on board for over 11 months had increased from 0.4 to

1.0 per cent.

Advances in international law and technology

The COVID-19 pandemic has interfered with international trade, creating inefciencies, delays and

supply-chain disruptions on an unprecedented scale – which also have legal consequences if contractual

performance is disrupted, delayed, or becomes impossible. For shipping this can lead to litigation that

raises complex international jurisdictional issues. Government and industry will need to work together

to address the related contractual rights and obligations, and arrive at standard contractual clauses for

commercial risk-allocation.

REVIEW OF MARITIME TRANSPORT 2021

xxii

Many of the problems are associated with delays in documentation – which should encourage more

commercial parties to adopt secure electronic solutions. Updated industry guidelines adopted recently,

offer useful guidance to shipowners and operators on procedures and actions to maintain the security

of IT systems in their companies and onboard ships, adopting a cyber-risk management approach, and

taking account of the IMO requirements, and other relevant guidelines.

Technological innovation is also raising the prospect of automated crewless vessels. The industry is

conducting trials on “maritime autonomous surface ships” (MASS). The aim is to ensure safe, secure and

environmentally sustainable shipping with the relevant legal framework. In May 2021, the IMO Maritime

Safety Committee completed a regulatory scoping exercise for the use of MASS which highlighted some

priority issues. The outcome could be a MASS instrument/code, with goals, functional requirements and

corresponding regulations, suitable for different degrees of autonomy.

On the path to a 3°C temperature rise

The shipping industry has an important part to play in combatting climate change. The Paris Agreement

aimed to reduce global warming to well below 2°C and pursue 1.5°C. But, despite a brief dip in carbon

dioxide emissions caused by the COVID-19 pandemic, the world is still heading for a temperature rise in

excess of 3°C this century. Urgent action is needed on both mitigation and adaptation.

At the regulatory level, the shipping industry is addressing climate issues through the 1973/1978

International Convention for the Prevention of Pollution from Ships (MARPOL). In June 2021, the IMO

adopted amendments to Annex VI of the Convention, which introduced new mandatory regulations to

further reduce greenhouse gas emissions from shipping, and require owners to set energy efciency targets.

There were also initial discussions on the mid- and long-term action needed, including market-based

measures, along with an industry-led proposal for an International Maritime Research and Development

Board a non-governmental body which would be nanced by a levy on marine fuel and would support

research, development, and the deployment of zero-carbon technologies.

Climate change, with the prospect of accelerating sea-level rise and more extreme weather events,

will also have major implications for the world’s seaports. Securing global maritime transport and trade

will therefore mean investing in adaptation and building resilience- for seaports and other key transport

infrastructure, especially in developing countries.

Broad-based global recovery will depend on smart, resilient and

sustainable maritime transport

The COVID-19 pandemic triggered a succession of shocks and waves, each setting off their own spinoff

events. The extent and impact of disruption varied considerably, however, between regions, economic

sectors, and segments of the shipping market. The recovery is similarly proving uneven, with differences

in the levels and scale of policy support and unequal access to vaccines.

Although the initial impact on maritime transport was less dramatic than predicted, the outlook is shadier.

The timescale for a lasting recovery will depend on the progress of the pandemic, the extent and timing of

world vaccination plans, and the duration of policy support measures. At present the nascent recovery is

being threatened by supply-chain breaks and logistical bottlenecks that are disrupting shipping markets

and pushing cost levels to historic highs.

The COVID-19 disruption has also accelerated pre-existing megatrends – geopolitical, technological, and

environmental. These trends have been unfolding slowly over the past decade but have accelerated

during the pandemic and continue to transform maritime transport and trade:

Geopolitics – The COVID-19 health crisis underscored the extent to which nations are economically and socially

interdependent – integrated through global supply chains and their underlying extended maritime transport networks.

In the face of heightened geopolitical risks and rising trade tensions, many countries and enterprises are shifting their

mindsets and now perceive global interdependency partly as a vulnerability. To mitigate risks and build resilience –

they are therefore aiming to reduce their reliance on distant foreign suppliers.

Resilience – The COVID-19 disruption has tested supply chains and their underlying business models, and put

transport and logistics networks under strain. Enterprises and governments are aiming to make supply chains more

robust and resilient, including by looking to diversify their business partners and suppliers. This will involve a new

balance between local, regional and global production. They are also reconsidering inventory and stock management

strategies and the trade-offs between just-in-time and just-in-case supply chain models.

REVIEW OF MARITIME TRANSPORT 2021

xxiii

Technology – Customs ofcials, port workers, and transport operators increasingly recognize the value of new

technologies and digitalization, not just as a way of boosting efciency but also for maintaining business continuity

at times of disruption. Technological innovations include advanced analytics, on-board sensors, communications

technology, port-call optimization, blockchains, big data, and autonomous ships and vehicles. During the pandemic,

these technologies have helped reduce physical contact, and keep ships moving, ports open and cross-border trade

owing. Technological advances have also stimulated consumer spending online and a growth in e-commerce. These

trends will continue to redene production and consumption patterns and the ways in which ships, ports and their

hinterland connections deliver cargo and services.

Shipping market dynamics – In anticipation of future disruptions, carriers, shippers, ports, and inland transport

operators will be rethinking their business and operating models to respond more exibly to changing market

conditions. Having seen the way in which the trade rebound stumbled against logistical bottlenecks and constrained