B.K.

GOEL

CHARTERED

& ASSOCTATES

ACCOUNTANTS

Phone:

401

58777. 4l

0 | ! 335

P-16,

N.D.S.E.

II I'r

Floor

NEW DELHI-110049

The

Boarci

of Eirectors

Sunflame

Enterprise

Private

Limited

Khasra

No,

7 2/4/7, Mundka

Industrial

Area

(North

Side)

Village

-

Ghevra

New Delhi

-

I1.004L

Report

on

special

purpose

financial

statements

1" This

report is

issued in

accordance with

the

terms of

our agreement.

2'

We have

audited

the accompanying

special

purpose

financial

statements

of Su;flame

Enterprises

Private

Limited

(the

"Company")

which

comprise the

balance

sheet

as at March

3L,2023,

and

the

statement

of

profit

and loss,

Statement

of Cash Flows

and

the statement

of changes

in

equity for

the

pei',od

January 12,

2023

to March

31, 2023 and

a summary

of

significant

accounting

policies

and

other explanatory

information,

which

we have

signed

under reference

to

this reperrt.

Management's

Responsibility

tor

the Financial

Statements

3. Management

is responsible

fer the

preparation

of these

special

purposc

finrn:i'lr

rtjhrnents

i1

accordance with

the Accounttng

Standards

specifierl rrnder

Section 133

of

the Co'np.anir:s

A.r:t, 20i

j

read

witlt Rule

7 of the

Companies

(Accounts)

Rul€s, 2AI4,tothe

extent

considered

relevurrt

by

;t

for

the

purpose

for

whrch

these special

purpose

financial

statements

have

been

prepared

(rhe

"accounting

principles

generally

accepted

in India").

The

responsibility

ineludes

the design,

implementation

and maintenance

of internal

control relevant

to the

preparation

of

special

purpose

financial

statements

that are free

from material

misstaternent,

whether

due

to fraud

or

error.

Auditor's

Responsibility

4.

Our responsibility

is to

express an

opinion

on these speeial

purpose

flnancial

statements

based on

our

audit" We

conducted

our

audit in accordance

with

the

Standards

on Auditing

specified

under

Section

143(10)

of the

Companies

Act,2013

("the

Act")

and

other

applicable

authoritative

pronouncements

issued

by the Institute

of

Chartered Accountants

of India.

Those

Standards

require

that we

comply

with

ethical requirements

a rd

plan

and

perform

the

audit

to obtain

reasonable

assurance

about

whether

the financial

statements

are free

from

rnaterial

misstate;,nent.

5' An

audit involves

perfornrii'rg

procedures

to obtain audit

evidence

about

the

amounts

and

disclosures

in

the special

purpose

finai:cial

statements. The

procedures

selected

depend

on

the auditors'

judgment,

including

the assessrnent

of the risks

of material misstaternent

of the finane

ial

statements,

whether

due

to fraud

or error.

In making

those risk

assessments,

the auditors

consider

internal

eontrol relevanttothe

entity's

preparation

and fair

presentation

of

the financial

statements

in

order

to design

audit

procedures

that

are appropriate

in the

circumstances,

but not for

the

purpose

of

'i

,r;fl

i.

ii

,{

h

B"K"

GOEL

& ASSOCIATES

phone:

40rs8777,410n33s

CHARTERED

ACCOUNTANTS

P-I6,

N.D.S.E,

II I.tFIooT

NEW DELHI-t7OO49

expressing

an

opinion on the

effectiveness

of the entity's internal

control.

Anr audit

also includes

evaluating

the

appropriateness

of accounting

policies

used

and the

reasonableness

of accounting

estimates made

by Management,

as well

as evaluating

the

overall

presentation

of

the financial

statements.

6. We

believe that

the audit

evidence we have

obtained is

sufficient and

appropriate

to

provide

a basis

for

our

audit opinion.

Opinion

7

"

Based

on

our audit, we report

that:

a. We

have obtained

all

the

information

and explanations

which,

to the

best of

our knowledge

and

belief, were

necessary

for the

purposes

of

our audit;

b" The Balance

Sheet,

Statement

of

Profit

and Loss,

Statement

of

Changes in Equity

and Statement

of Cash

Flows dealt with

by this report

are in

agreement with

the

books

of account;

c. ln

our opinion

and to the best

of our information

and

according

to the

explanations

given

to us,

the

specialpurpose

financialstatements,

togetherwith

the notes

thereon

and

attached

thereto,

fairly

present,

in

all material

respects, in

conformity

with

the accounting

principles

generally

accepted

in India:

(i)

in

the

case of the Balance

Sheet,

the state of

affairs of the

Company

as at March

3I,2023;

(ii)

inthecaseof

theStatementof

Profitand Loss,the

profitforthe

periodJanuary

12,2}23to

March

31,2023;

(iii)

in

the case

of Statement

of Changes in Equity,

of the

change in

equity for

the

period

January

12,

2A23

b March

3I,

2A23;

and

(iv)

in

the case of

the Statennent

of eash Flows,

of the eash flows

forthe

period

ended March

31,2023"

Other Matter

8. The

special

purpose

financial

statements

dealt with

by this report,

have

been

prepared

for

the

express

purpose

to

enable the

Group auditor's

(PWe)

to

express

opinion

on eonsolidated

finaneial

statements

of

V-Guard

group

for the

year

ended Mlarch

31,2A23

pursuant

to

the agreement

between

the Company

and B.K. Goel

&

Associates.

Restriction

sn

Use

9. Our obligations

in respect

of this report

are entirely

separate from,

and

our responsibility

and liability

is in no way

changed

by, any

other role we rnay

have

(or

may

have

had)

as auditors

of the

Company

l^

Phone:

40158777,

410l 1335

P-16,

N.D.S.E.

II I't Floor

NEW DELHI-110049

or

otherwise. Nothing in

this report,

nor

anything said or

done in the

course

of or in connection

with

the

services

that are the subject

of this report,

will extend

any

duty of

care we may have

in

our

capacity

as auditors of any financial

statements of

the Company.

10. This

report is

addressed

to the Board

of

Directors

of the Company

and

has been

prepared

for

and

only for

the

purposes

set out in

paragraph

8 above.

This report

should

not be

othenryise

used

or

shown

to or

otherwise distributed

to any

other

party

or used for

any other

purpose

except with

our

prior

consent

in writing. B.K

Goel

&

Associates

neither

accepts

nor assumes

any

duty, responsibility

or liability

to any other

party

or for

any other

purpose.

For

B.K

Goel & Associates

Firm Registration

No:

016642N

Accountants

B.K.

GOEL

& ASSOGIATES

CIIARTERED

ACCOUNTA}ITS

Place:

Gurugram

Date:15.05.2023

B.K

Goel

(Proprietor)

Membership

No:

082081

U>)N

19a

*to&l

(t|wtl-

FA

aQtg

Sunflame

Enterprises Private

Limited

Special

Purpose Financial

Statement as at March

31, 2023

(Amount

in t lakhs, unless

otherwise

stated)

Particulars

Notes

As at

March 31. 2()23

Opening

as at

January

12,2023

Assets

Non-current

assets

Property,

plant

and

equipment

Right-of-use assets

Investment

ProperW

Other

intangible assets

Financial assets

Investments

Loans

Deferred tax assets

(net)

Other

non-current assets

Total non-current assets

Current

assets

Inventories

Financial

assets

Trade

receivables

Cash

and cash equivalents

Other bank

balances

Current tax

asseG

(net)

Other

current assets

Total current assets

Total Assets

Equity and

liabilities

Equity

Equity share

capital

Other equity

Total Equity

Liabilities

Non-current

laabilitaes

Financial

liabilities

Lease liabilities

Provisions

Other

non-current liabilities

Total non-cu

rrent

liabilities

Current

liabilitaes

Financial

liabilities

Lease liabilities

Trade

payables

Total

outstanding

dues of micro enterprises

and small enterprises

Total outstanding dues of credatoG other

than micro enterprises

and

small enterDrises

Other

current liabilities

Current

tax liabilities

(net)

Provisions

Total current

liabilities

Total liabilities

5

9

10

11

11

LZ

13

t4

4,209.94

220.52

150.00

2.44

0.45

400.00

34.97

15.36

4,247.4a

'

150.00

o.45

400.00

33.7r

15.38

6

7

31

B

ao

L7

18

5,()33.72

4,a5(J.39

3,642.84

3,358.85

634.83

2,688.33

39.40

184.59

3,274.L3

4,297.97

138.98

474.65

L27.99

124.72

10,544.44

15,542.56

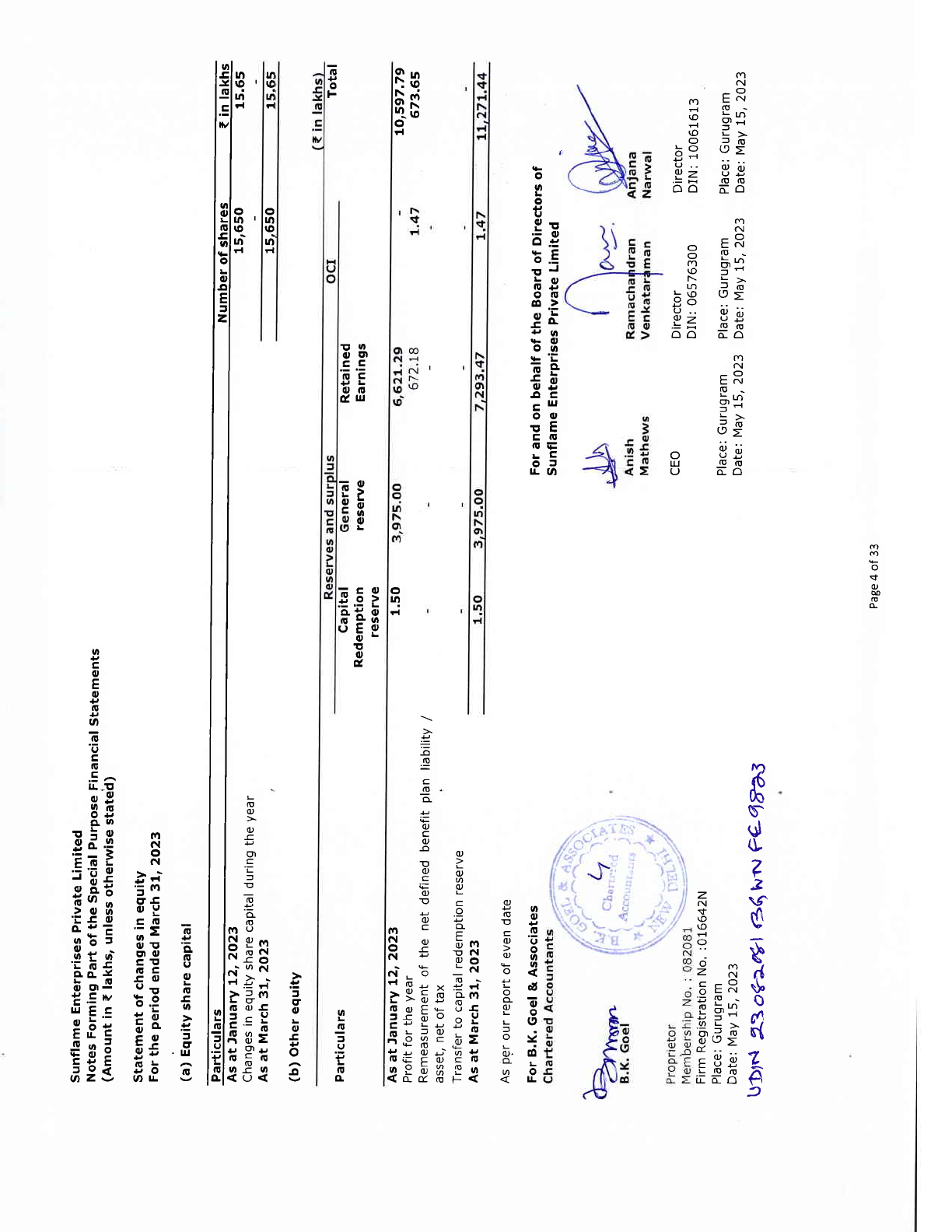

15.65

tL277.44

tl,2a7.o9

720.24

18.36

168.69

307.29

LOt.70

3,334.2t

489.69

55.47

7.tr

3,988.18

4.295.47

Board of Directors

of

Place:

Gurugram

Place:

Gurugram

Date:

May 15,2023

Date: May L5,2023

8.772-3A

13.622-77

1( Aq

10.597, t9

1o,613.44

20.42

1 69.1 6

149.94

16

19

20

22

L,626.22

L,t44.76

4.37

2,819.3s

3.OO9-33

Membershio

No. :

082081

Firm Registration No. :016642N

Place:

Gurugram

Date:

May L5,2023

Narwal

Darector

DIN:10061613

Place:

Gurugram

Date: May

L5,2023

Total equity and liabilities

The accompanying

notes

are an integral

part

of the special

purpose

financial statements.

As

per

our

report of

even date

For B.K. Goel &

Associates

Chartered

Accountants

For and

o

Sunflame

Anish

Mathews

cEo

#':E'S

K-,{

8(

c)

{;-r#.

UD,sr

-S

UeIo*)

N)v{N

ee

4€23

Page

1 of 33

Sunflame

Enterprises Private

Limited

Speciaf Purpose

Financial

Statementfor the

period

January L2,2023

to March

3L,2023

(Amount

in t lakhs, unless otherwise

stated)

(<

an lakhs)

For

the

period

Particufars

Notes

tanuary

!2,20.22

to March 3L,2'J23

Revenue

Revenue from ooerations

Other income

Total income

Expenses

Cost of

materials consumed

Purchases of

Finished Products

Changes

in Inventories

Employee benefits expense

Finance costs

Depreciation

and amortization

expense

Other expenses

Total

expenses

Profit/(loss) before exceptional items and

tax

Exceptional

ltems

Profit before tax

Current

tax expense

Income tax adjustment

related

to

prior years

Net deferred

tax benefit

Income tax expense

Profit after tax

Other comprehensive

income

A. Items that

will not be reclassified

to

profit

or loss

Re-measurement

losses on defined

benefit

plans

Tax imDact on above

B. Items that

wall be reclassified

to

profit

or loss

Total other comprehensive

gain

for

the

year,

net of

tax

Total comprehensive

income

for the

year

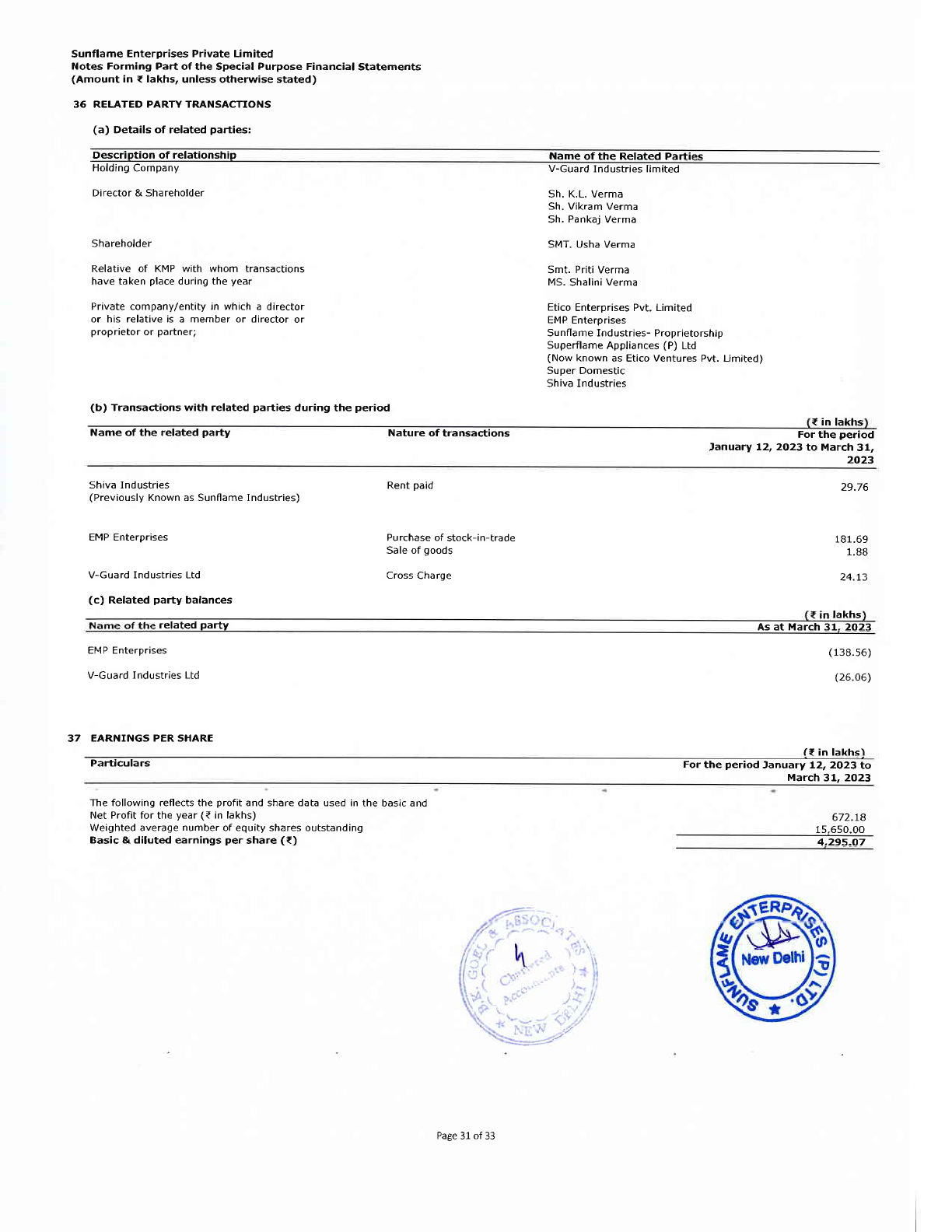

Earnings

per

equity share:

Basic and diluted

The accompanying

notes are an Integral

part

of the financial statements.

As

per

our

report of even date

For B.K. Goel

& Associates

Chartered

Accountants

Propraetor

Membershio

No. : 082081

Firm Reoistration

No. :016642N

23

24

25a

26

25b

27

2A

29

30

ry-

5,690.10

46.)'l

s,736.31

1,340.85

2,600.35

(4s2.9e)

243.24

4.63

93.a7

973.89

31

4.443-44

892.47

'392.47

222.O5

(t.761

220'29

672.r8

1.95

{o.49)

1.47

4,295"07

Narwal

Director

DIN:10061613

Place:

Gurugram

Date: May

75,2023

1.47

Place: Gurugram

Date: May 15,2023

ub|sr

z1oh.o&l

b6,w*Fa

qhs

,67

Q*;9

andran

raman

Director

DIN: 06576300

Place:

Gurugram Place: Gurugram

Date:

May 75,2023 Date: May

75,2023

Ramac

Page

2 of 33

Sunflame Enterprises Private

Limated

Speciaf Purpose

Financial

Statement

for the

period

tanuary 12, 2023

to March 31, 2023

(Amount

in t lakhs, unless

otherwise stated)

Particulars

For

the

period

January 12,2(J23

to March 31,2(J23

Cash

flow from operating

activities

Profat

before tax

Adjustment to reconcile

profat

before

tax to net cash flows

Depreciation and amortization expense

Finance

cost

Finance income

Operating

profit

before working

capital

changes

Movements

in working

capital?

Trade

payables

In ventory

Current tax liabilities

(net)

Deferred tax assets

(net)

Provisions

Current tax assets

(net)

Trade receivables

Other non current

liabilities

Other current liabilities

Other current assets

Other non current

assets

Cash

generated

from

operations

Direct taxes

paad

(nel

of

refunds)

Net cash

generated

from

operating activities

(A)

Cash flows from investing actavaties

Net sales/(Purchases) of

property, plant

and equipment,

including CWIP

Investments in bank deposits

(net)

Interest received

Net

cash

generated

from/(used

in) anvesting activities

(B)

Cash flows from financing activities

Lease Payments

made during

the

year

Other interest costs

Net

cash

used in fanancing activities

(C)

Net decrease an cash and cash equivalents

(A+B+C)

Cash and cash equivalents at the beginning of

the

year

Cash

and

cash equivalents at

the end of the

year

The accompanying noteJare an integral

part

of the special

purpose

financial

statements.

492.47

93.47

4.63

(38.67)

952.30

7,707

.99

(428.71)

55.47

(r.26)

(2.26)

82.60

939.06

(0.47)

(6es.07)

(ss.87)

0.02

2F49.8O

(220.291

2.329-51

(2e.t2)

(

1,813.68)

38.68

(1,804.12)

(2e.3e)

(0.1

5)

(29-S4l

495.85

138.98

634.43

For B.K. Goel & Associates

Chartered Accountants

\-

A}rfi\.nm/-

B.K. Goel

Proprietor

Membership

No. :

082081

Firm Registration No. :01664iN

.,-

-

Place: Gurugram

Date: May 15,2023

UDrs

*ogA.o&f

rD6,X

tv

For and on

behalf of the Eoard

of Directors of

Sunflame Enterprises

Private Limated

lA

4

dran

man

CEO Director

Director

DIN: 06576300

DIN:10061613

Place:

Gurugram Place:

Gurugram

Place: Gurugram

Date:

May t5,2023 Date:

May 15,2023 Date:

May 15,2023

Ramacha

FO

48a3

Page

3 of 33

cn

N

_o

FN

;;

L6

6

:>

o

lo

xo

(,>

U

--

nr ;:

9z

6.Y

UU

LU

m

C\l

-o

o

trc{

m

=d

N

=>-

tr)J6

bP

cr:

u

..

oJ ;i

g)7

Ui:

.=F

o

G

oo

6:o

rr)

N

-o

IN

l

=>

.=o

u/>

i4;

UOG

u a:o

$u

il$

I

o

o

o

u

u

EJ

etr

o.:

EJ

hg

oo

t0

.:

;A

Pvl

sC,

O('

s'i

E9

5g

llc

-uJ

oo

sE

trlu

t!

i=

LL

OJ

trUl

o

st

o

@

@

c

o

4

=

-o

.o

l1,l

t6

0o

s

,ul

(L

7

3

K\t

g$

5T

;

-B

ziiirl

F ER $

*q;

o

-b

5'i

A

a;F'(

tsn z

r-#E

F

2

c

o-

=

a

a

-oo

xL

zg

c)L

!:g.n

E E

€g

m-o

q!

c.r F-

q'l

'O

R

E

iil

d

3

ri.b

jx

b

i

*fr.-Ej

! d

lxbp *oo

3

='

t!otrs

UE I X

:5F9eg

:6

:

=fi

-

G

f

ripB;&E

3

X

t#E6EE

g'T

{,ieHEt &

E

t

u

o

Elo

ogl

oc

oo

d,u

o

I

tu

o

o

EEi

.s"s$

o-

It

o

d

IE

L

o

It

L

3

l

L

o

o.

.:

a

c'

o

L

o

o

.Ct

l;lll

lq--

ll

tl

Pll

fI

E"ll

[g

| |

q

E*:

H

IIF

lgiEgnll,F,

gigEiilfligi

Sunflame

Enterprises Private Limited

Notes Forming

Part ofthe Financaal

Statements

(Amount

in { lakhs, unless otherwise

stated)

CIN No.

: U74899DL1984PTCO18992

2.2

2.1

CORPORATE

INFORMATION

Sunflame

Enterprises Private

Limited

(hereinafter

referred

to

as

'SEPL'

or 'the

Company')

is

a

private

limited

company

domicifed

in India with its registered

office

at

Khasra

No.

72/4/7, Mundka Industrial

Area

(North

Side)

Village

-

chevra, New

Delhi- 110041.

The

Company was incorporated on August 27, 7984.

The Company

is engaged in manufacturing

and selling

kitchen

appliances in India.

Company's

product portfolio

includes a wide

range of kitchen

appliances such as

gas

stoves,

cooktops,

chimneys,

induction cookers, electric cookers, and more. The

Company's manufacturing

facility is located

at IMT,

Fa rida

bad.

SIGNIFICANT

ACCOUNTING

POLICIES

This note

provides

a list of the significant accounting

policies

adopted in the

preparation

of these Indian Accounting

Standards

(Ind

AS) financial statements. These

policies

have

been consistently applied

to all the

years

except where

newly issued

accounting standard is initially adopted.

Basis of

preparation

of financial statements

The

financial statements

of the Company

have

been

prepared

in

accordance with Indian Accounting

Standards

(Ind

AS)

notified under Companies

(Indian

Accounting

Standards) Rules, 2015

(as

amended from time

to time) and

presentation

requirements of Division II of Schedule III to the

Companies

Act, 2013.

The

financial statements have

been

prepared

on a historical cost basis, except

certain financial assets

and liabilities that are

measured at fair value.

The

financial

statements are

presented

in

Indian Rupees

('t').

These Values

are

also

rounded

to nearest lakhs upto

two

decimal

places ({00,000),

except

when

otherwise

indicated.

Summary

of sagnificant accountang

policies

a)

Current versus non-current classificataon

The Company

presents

assets

and

liabilities in

the Balance Sheet based

on current

/

non-current

classification. An asser ts

treated

as current when it is:

.

Expected to be realized or intended to be sold

or consumed

in

normal operating

cycle

.

Held

primarily

for the

purpose

of trading

.

Expected to

be realized within

twelve months after the reporting

period,

or

.

Cash

or cash equivalent unless restricted from

being exchanged or used

to settle a liability for

at

least

twelve months after

the reporting

period.

All other

assets are

classified as

non-current.

A liability

is

current when:

.

It

is

expected

to be seEtled in normal

operating cycle

.

It is held

primarily

For the

purpose

of trading

.

It is due to be settled within twelve months

after the

reporting

period,

or

.

There is no unconditional right to defer the

settlement of the liability For

at least twelve months after the reporting

period.

All other

liabilities are classified as non-current.

Deferred tax assets and liabilities are classified as non-current

assets and liabilities.

The operating cycle is the time between the acquisition

of assets for

processing

and their realization in

cash and cash

equivalents.

The Company has identified

twelve months as its operating

cycle.

b) Foreign

currencaes

The

Company's

financial statements are

presented

in

Indian Rupees

('{')

which is

also the Company's lunctional

currency.

Transactions and balances

Transactions in Foreign currencies are initially recorded

by the Company

at their respective functional

currency spot rates at

the date the transaction

first

qualifies

for recoqnition. However, for

practical

reasons,

the Company uses an average rate ifthe

average

approximates the actual rate

at the date of the transaction.

Page

5 of 33

Sunflame

Enterprises

Private

Lim:ted

Notes Forming

Part ofthe Financial

Statements

(Amount

in t lakhs, unless otherwise stated)

CIN No. : U74899DL1984PTCO18992

Monetary assets and liabilities denominated in foreign currencies

are translated

at the tunctional currency

spot rates of

exchange

at

the

reporting

date. Exchange differences arising

on settlement or translation

of monetary items

are

recognised

in

the Statement

of Profit

and

Loss.

Non-monetary

items

that are

measured in

terms of historical cost in

a

foreign

currency are

translated using the

exchange

rates at the dates of the initial

transactions.

Non-monetary

items measured

at

fair value

in a foreign

currency are translated

using the exchange rates at the date when

the

fair value is

determined. The

gain

or loss arising

on translation oF non-

monetary

items

measured at fair value is treated in line with

the recognition ot

the

gain

or loss on the

change in fair value of

the item

(i.e.,

translation differences on items whose fair value

gain

or loss is recognised in

OCI or Statement

of

Profit

and

Loss

are also recognised in OCI or

Statement

of Profit and

Loss, respectively).

c) Fair

value measurement

Fair

value is the

price

that would

be

received

to sell an asset or

paid

to transfer a liability in an

orderly transaction between

market

participants

at the measurement date. The

fair

value

measurement is

based on the

presumption

that the transaction

to sell the

asset or

transfer the

liability

takes

place

either:

.

In the

principal

market For asset or liability, or

.

In

the absence of a

principal

market, in then most

advantageous market for

the asset or liability.

The

principal

or the most advantageous market must

be

accessible

by the Company.

The

fair

value

of an asset or liability is measured

using the assumptions

that market

participants

would use when

pricing

the

asset

or

liability,

assuming that market

participants

act

in

their economic best interest,

A fair

value measurement

of a

non-financial

asset takes into account

a market

participant's

ability to

generate

economic

benefits

by using the asset in its highest and

best use or by selling it to another

market

participant

that would

use the asset in

its

highest and best use.

The Company uses

valuation

techniques that are appropriate

in the circumstances

and for which sufficient data

are available

to measure

fair value, maximising

the use of relevant observable inputs

and minimizing

the use of unobservable inputs.

All assets and liabilities

for which fair value

is measured or disclosed

in the financial

statements are categorized within

the

Fair

value hierarchy, described as follows, based on

the lowest level input that is

significant to the fair value measurement

as a

whole:

.

Level 1

-

Quoted

(unadjusted)

market

prices

in

active markets for identical

assets or liabilities

.

Level

2

-

Valuation

techniques

for which

the lowest level input

that is significant

to the

fair value

measurement is directly

or

indirectly

obseruable

.

Level 3

-

Valuation techniques for which the lowest level

inout that is

siqnificant to the fair value measurement is

unobservable.

For assets

and liabilities that are recognised in

the

financial

statements

on a

recurring

basis, the

Company determines whether

transfers

have

occurred between levels in the hierarchy

by

re-assessing

categorization

(based

on the lowest level input

that

is

significant

to fair value

measurement as a whole) at the end

of each reporting

period.

d)

Revenue

Revenue

from contract wath

customers

-

Revenue

from contracts

with

customers is recognised when

control ofthe

goods

are transferred to the customer

at an amount

that

reflects the consideration to

which

the Company

expects to be entitled in

exchange for those

goods

or services. The

Company

has

generally

concluded that it is

the

principal

in its revenue arrangements

because it typically

controls the

goods

or

services

before transferring them to the customer.

(i)

Sale

of

products

Revenue

from

sale of

products

is recognised at

the

point

in

time

when

control

of the asset is transferred to

the customer,

generally

on delivery of the

products

to customer's

premises.

Company deals

primarily

with Super-distributors

(General

trade),

Canteen

stor€s, Police canteens, Modern retails, Institutional

buyers & E-commerce

platforms.

The normal credit

term

is

7 to

60 days

upon

delivery

of

goods.

The Company

considers whether there are other

promises

in the contract that

are separate

performance

obligations

to

which

a

portion

of the transaction

price

needs

to be allocated if any. In

determining

the transaction

price

for the sale of

goods,

the

Company considers

the

effects of

variable

consideration,

the existence of

significant financing components, non-cash

consideration,

and consideration

payable

to the customer

(if

any).

Page

6 of l3

w

Sunflame

Enterprises Private Limited

Notes Forming

Part

ofthe Financial Statements

(Amount

in { lakhs, unless otherwise

stated)

CIN No, ? U74899DL1984PTCO1a992

Variable consideration

If

the

consideration in

a contract

includes

a variable

amount, the Company

estimates the amount

of consideration

to

which

it

will be entitled in exchange for transferring

the

goods

to

the customer.

The variable

consideration is

estimated at contract

inception and constrained

until

it is

highly

probable

that a significant revenue reversal

in the

amount of cumulative revenue

recognised

will

not occur when

the associated uncertainty with

the variable

consideration is

subsequently resolved. The

contracts for the sale of

goods provide

customers with a right

of return, cash

discounts and volume

rebates/trade incentives,

The rights of return, cash discounts and volume

rebates/ trade incentives

give

rise

to

variable

consideration.

Volume

rebates

The

Company

provides

retrospective volume

rebates

/

trade

incentives

to

customers once the

quantity

of

products purchased

during

the

period

exceeds a threshold

specified in the

contract. Rebates are

offset against amounts

payable

by the customer.

The Company estimates the variable

consideration for

the

expected

future rebates

/

trade incentives

based on its experience

of the expected

value,

The Company then

applies the requirements

on constraining estimates

of variable consideration,

Trade receivables

A

receivable represents

the Company's right

to

an amount

of consideration

that is unconditional

(i.e,,

only the

passage

oftime

is required before

payment

of the consideration is due).

contract liabilitaes

A contract liability

is

the obligation to transfer

goods

or services

to a customer for which

the Company has received

consideration

(or

an

amount of consideration is due) from

the customer. If

a customer

pays

consideration before

the Company

transfers

goods

or services to the

customer, a contract liability is

recognised when

the

payment

is made

or the

payment

is

due

(whichever is

earlier). Contract liabilities are recognised

as revenue when

the Company

performs

under the contract,

(ii)

Assets and liabilities arising from rights

of return

Raght of return assets

Riqht of

return

asset represents the

Company's right to recover

the

goods

expected

to be returned by customers.

The asset is

measured at the

former

carrying amount of

the

inventory,

less any

expected costs to recover

the

goods,

including

any

potential

decreases in

the

value

of the

returned

goods.

The

Company updates

the

measurement

of

the asset recorded tor

any

revisions to its expected level of returns,

as well as any

additional decreases in

the

value

of the returned

products.

Interest income

For all

debt instruments measured

either at

amortised cost or at fair value

through other comprehensive

income, interest

income is recorded usinq the effective interest

rate

(EIR).

EIR is

the rate

that exactly discounts

the estimated future

cash

payments

or receipts over the expected life

oF the financial instrument

or a

shorter

period,

where appropriate,

to the

gross

carrying

amount

of the

financial

asset or to

the amortised cost of

a

financial

liability. When

calculating the effective

interest

rate, the Company estimates

the expected cash flows by

considering all the contractual

terms of the financial

instrument

(for

example,

prepayment,

extension,

call and similar options)

but does not consider

the expected credit

losses. Interest income is

included

in finance income

in the Statement

of Profit and Loss.

Dividends

Revenue is recognised when

the Company's right

to

receive

the

payment

is

established, which is

generally

when shareholders

approve

the dividend.

e) Taxes

current income tax

Current

income

tax assets and liabilities

are

measured

at the

amount expected to be recovered from

or

paid

to the taxation

authorities.

The tax rates and

tax

laws

used to compute

the amount are

those that are enacted or

substantively

enacted, at

the

reporting date.

Current

income tax relating

to

items recognised

outside

the Statement

of

Profit

and Loss is recognised

outside the Statement

of

Profit and Loss

(either

in

other comprehensive income

or equity). Current

tax items are recognised in

correlation

to the

underlying transactions either in OCI or directly

in equity.

Management

periodically

evaluates

positions

taken in the tax returns with

respect

to

situations

in which applicable

tax

regulations are subject to interpretation

and considers whether

it is

probable

that a taxation authority will

accept an uncertain

tax treatment.

The

Company shall reFlect

the effect of uncertainty for

each uncertain

tax treatment by using either most

likely

method

or expected value

method, depending

on

which

method

predicts

better resolution

of the

treatment.

Page 7 of 33

Sunfl ame

Enterprises Private Limited

Notes Forming

Part of

the

Financial

Statements

(Amount

an { lakhs,

unless

otherwise stated)

CIN No.

I U7 4899DLL9a4PTCO18992

Deferred tax

Deferred

tax is

provided

on temporary differences between the tax bases

of assets and liabilities

and their carrying amounts

for financial

reporting

purposes

at the

reporting date.

Deferred

tax

liabilities are

recognised for

all taxable temporary differences,

except:

.

When

the deferred

tax liability

arises

From the initial recognition of

goodwill

or an asset or liability in

a transaction that is not

a business

combination and, at the

time

of

the transaction, affects neither

the

accounting

prorit

nor taxable

profit

or

loss,

.

In respect of taxable temporary differences associated with investments

in subsidiaries,

associates and interests in

joint

ventures,

when

the timing ofthe

reversal

ofthe temporary differences

can be controlled and it is

probable

that the temporary

differences

will not reverse in the Foreseeable future.

Deferred tax assets are recognised for all deductible temporary

differences, the carry forward

of unused tax credits and any

unused

tax losses. Deferred

tax

assets

are recognised to the extent

that

it is

probable

that

taxable

profit

will be available

against

which the deductible temporary differences,

and the carry forward of unused

tax credits and unused

tax losses can be

utilised,

except:

.

When

the deferred tax

asset

relating

to the deductible temporary difference

arises from the initial recognition

of an asset or

liability

in a transaction that is not a business

combination and, at the time of

the transaction, affects neither

the accounting

profit

nor taxable

profit

or loss.

.

In respect of deductible temporary differences associated with investments

in subsidiaries,

associates and interests in

joint

ventures, deferred tax assets are recognised only to the

extent that it is

probable

that

the temporary differences will reverse

in the

foreseeable future and

taxable

profit

will be available against which

the temporary differences

can be utilised.

The carrying

amount of deferred

tax assets

is

reviewed at each reporting date

and

reduced

to

the

extent

that

it is no

longer

probable

that sufficient taxable

profit

will

be available to allow all or

part

ofthe deferred tax asset to be

utilised. Unrecognised

deferred

tax assets are re-assessed

at each reporting date and are recognised

to the extent

that

it has

become

probable

that

future

taxable

orofits

will allow the deferred

tax asset to be recovered.

Deferred tax

relating

to

items recognised

outside

profit

or

loss

is

recognised outside

profit

or loss

(either

in other

comprehensive

income or in equity). Deferred

tax items are recognised in

correlation to the underlying

transaction either in

OCI or

directly in equity.

Deferred tax assets and liabilities are measured

at

the tax rates

that are expected to apply in

the

year

when the asset is

realized

or the liability is

settled, based on tax rates

(and

tax laws)

that

have

been enacted or substantively

enacted at the

reporting

date.

Deferred tax assets and deferred tax liabilities

are offset

if

a legally enforceable right

exists to set off current

tax assets

against current

tax liabilities and the

deferred taxes relate to the same

taxable entity and the same taxation

authority.

Goods

and services taxes

paid

on acquisation

of

assets

or on Incurrtng expenses

Expenses

and assets are recognised net of

the amount of

goods

and seruices

taxes

paid,

except:

.

When the tax

incurred on a

purchase

of assets or services is not recoverable from

the taxation authority, in which

case, the

tax

paid

is recognised as

part

of the

cost of acquisition of the asset or as

part

of the expense item, as applicable.

.

When receivables and

payables

are stated with

the

amount

of tax included.

The

net amount of tax recoverable from,

or'payable to, the taxation

authority

is included

as

part

of receivables

or

payables

in

the

Balance Sheet.

f) Property,

plant

and

equipment

Property,

plant

and equipment are stated

at

cost, net

of accumulated depreciation

and accumulated impairment

losses, if any.

Capital

work-in-progress is

stated at cost, net of accumulated impairment

loss, it any. The

cost comprises of

purchase price,

taxes,

duties,

freight

and other incidental expenses

directly attributable and related

to acquisition and installation

of the

concerned

assets and are further adjusted by the amount

of tax credit availed wherever applicable.

When significant

parts

of

plant

and equipment are required

to be

replaced

at intervals,

the Company depreciates them separately

based on their

respective useful

lives.

Likewise, when a major inspection

is

performed,

its cost is recognised in

the carrying amount

of the

plant

and

equipment as a replacement if

the recognition criteria

are satisfied. All other repair and maintenance

costs are

recognised

in Statement of Profit and Loss as incurred.

An

item oF

property, plant

and equipment and any

significant

part

initially recognised is

derecognised upon disposal

or

when

no future

economic benefits are

expected from its use or

disposal.

Any

gain

or loss arising on

derecognition of the asset

(calculated

as the dirference between

the

net

disposal

proceeds

and the carrying amount of the asset) is included

in the

income statement

when

the asset is derecoqnised,

\-

Page

8 of 33

Sunflame

Enterprases Private Limated

Notes Forming

Part ofthe Financial Statements

(Amount

in t

lakhs,

unless

otherwise

stated)

CIN No.

: U74899DLl9a4PTCO1a992

Capital

work-in-progress includes

cost of

property,

plant

and equipment

under installation

/

under

development as at the

Balance

Sheet date.

The residual

values,

useful lives and methods of depreciation of

property,

plant

and equipment

are reviewed at each financial

year

end

and adjusted

prospectively,

if appropriate.

Depreciation on

property, plant

and equipment is calculated on a written

down value basis

using the rates arrived at

based on

the useful

lives

estimated by the management. The Company identifies

and determines cost

of each component

/

part

of

the

asset separately,

if the component

/

part

has

a cost

which is

significant to

the total cost of the

asset

having

useful life that is

materially different trom that of the remaining

asset,

These

components are depreciated

over their useful lives;

the

remaining

asset

is depreciated over

the life

of

the

principal

asset.

The Company

has used

the

following

useful lives to

provide

depreciation

on

its

property, plant

and

equipment:

Asset Cateoorv Useful

life

estimated bv the manaoement

(in

vears)

Factory

land NA

Factory

Building

30

Plant &

Machinery

15

Electrical Installations 15

Furniture

& Fixtures 10

Lab

Equipment 10

Motor

Vehicles 8

Office

Equipment

5

ComDuter

Hardware

3

g)

Investment

properties

Property

that is held for long term rental

yields

or

for

capital appreciation

or

for

both, and that is not

occupied by the

Company,

is classified as investment

property.

Investment

property

is measured initially

at its cost, including related

transaction cost and

where

applicable, borrowing costs. Subsequent

to

initial

recognition, investment

properties

are stated

at

cost less

accumulated deprecaation

and accumulated

impairment

loss, if any,

Subsequent expenditure is capitalised

to asset's

carrying

amount only when it is

probable

that

future

economic benefits associated

with the expenditure will

flow to the

Company

and the cost of the item can be measured reliably. All

other repair and maintenance

cost are expensed when

incu rred.

Investment

properties

are de-recognised

either when they have been

disposed off or when they

are

permanently

withdrawn

from

use and no future economic benefit is

expected

from

their disposal. The

difference between the net disposal

proceeds

and

the carrying amount of the asset is recognised in

Statement of Profit and Loss in

the

period

of de-recognition.

h) Intangible

assets

Intangible assets acquired separately are measured on initial recognition

at cost. Following initial recognition,

intangible assets

are carried

at cost less any

accumulated amortisation and accumulated impairment

losses. Internally

generated

intangibles,

excluding

capitalised development costs, are not capitalised

and the

related

expenditure is reflected

in the Statement

of

Profit

and

Loss in the

Deriod

in which

the exDenditure

is

incurred.

Cost comprises

the

purchase

price

and any attributable cost ot bringing

the asset to its working

condition

For

its intended use.

The useful

lives

of

intangible

asseG are assessed as either finite

or indefinite. Intangible assets with

finite lives are

amortised

over their

useful economic

lives and assessed for impairment whenever

there

is

an indication that

the

intangible

asset may be

impaired.

The amortization

period

and

the

amortization method for

an intangible

asset

with

a finlte useful

life

is reviewed

at

least

at the end of each

reporting

period.

Changes

in

the expected useful life or the

expected

pattern

of consumption of future

economic benefits embodied in

the asset

is

accounted for by changing the amortization

period

or method, as appropriate

and are treated as changes in

accounting

estimates.

The amortization

expense on intangible assets with finite lives

is recognised in the

Statement of Profit and Loss.

Intangible

assets with indefinite

useful lives are not amortised, but are

tested for impairment annually, either individually

or at

the

cash-generating unit level. The assessment

oF

indeFinite

liFe is reviewed annually

to determine whether the indefinite

liFe

continues

to be supportable. If not,

the change in useful life from indefinite

to finite is made on a

prospective

basis.

An intangible asset

is de-recognised

upon disposal

(i.e.,

at

the

date

the

recipient

obtains control)

or

when

no future economic

benefits

are expected from

its use or disposal. Gains or losses

arising

from

disposal of the intangible

assets are measured as

the

difference

between

the

net

disposal

proceeds

and

the carrying amount ofthe asset and are recognised

in the Statement

of

Profit and

Loss

when

the assets

are

disoosed.

Software

is amortized over

an estimated useful life of 3 vears.

Page

9 of 33

Sunflame

Enterprises Private Limated

Notes Forming Part ofthe Financaal Statements

(Amount

in t lakhs, unless otherwase stated)

CIN No. : U74899DLL984PTCO18992

i)

Borrowing costs

Borrowing costs directly attributable to the acquisition, construction

or

production

of an asset that necessarily

takes a

substantial

period

of

time to

get

ready for its intended use

or sale are capitalised as

part

of the cost of the asset. All other

borrowing costs are expensed in the

period

in which they occur. Borrowing

costs consist of interest

and

other

costs that an

entity

incurs in connection with the borrowing of funds. Borrowing

cost also

includes

exchange differences

to the extent

regarded as an adjustment to the borrowinq costs.

j)

Leases

The Company assesses at contract inception whether a contract is,

or contains, a lease. That is, if

the contract conveys the

right to control the use of an identified asset for a

period

oF time in exchange for

consideration.

Company

as a

lessee

The

Company's

lease asset class

primarily

comprise

of lease for

land and buildings. The Company

assesses

whether

a contract

contains a lease, at

inception

of a contract.

A

contract

is,

or contains, a lease if

the contract conveys the right to control

the

use of an

identified asset for

a

period

of time in exchange for consideration. To assess whether

a contract conveys

the

right

to

control the

use oF

an

identified

asset, the Company assesses

whether:

(i)

the contract involves

the use of an identified

asset

(ii)

the Company has substantially all of the

economic

benefits from

use of the asset through

the

period

of the lease and

(iii)

the

Company has the right to direct the use oFthe asset.

The Company

applies a

single

recognition

and

measurement

approach for all leases. except for

short-term

leases

and leases

of

low-value assets. For these short-term and low-value leases,

the Company recognizes the lease

payments

as an operating

expense on a straight-line basis over the term of the lease. The

Company

recognises

lease liabilities to make

lease

payments

and

right-of-use

assets

representing

the right to use the underlying assets.

i)

Right-of-use assets

The Company

recognises right-of-use

assets at the commencement date of the lease

(i.e.,

the date the underlying

asset is

available

for use). Right-of-use assets are measured

at cost, less any accumulated depreciation and impairment

losses,

and

adjusted

for any remeasurement oF lease liabilities. The cost of right-of-use

assets includes the amount

oF lease liabilities

recognised,

initial direct

costs

incurred,

and lease

payments

made at or before

the commencement date

less any lease

incentives received. Right-of-use assets in

the

nature

of buildings are depreciated on a s[raight-line

basis over the shorter

of

the

lease term and the estimated useful lives ofthe underlying

asset. The right-or-use assets

comprising

ofland

is depreciated

based

on the lease term.

If ownership

ot

the

leased asset

transfers to the Company at the end of the lease

term or the cost

reflects

the exercise

of a

purchase

option, depreciation is calculated using the estimated useful

life oF the asset.

The

right-of-use assets

are also subject to impairment, Refer to the accounting

policies

in

section

(l)

Impairment

of

non-

financial assets.

ii) Lease

Iiabilities

At the commencement date of the lease, the Company recognises lease liabilities measured

at the

present

value

of lease

payments

to be made over

the lease term.

The

lease

payments

include fixed

payments

(including

in

substance fixed

payments)

less any lease incentives receivable, variable lease

payments

that depend on an index or a rate,

and amounts

expected

to be

paid

under residual value

guarantees.

The

lease

payments

also include the exercise

price

oF

a

purchase

option

reasonably certain to be exercised by the Company and

payments

of

penalties

for terminating the lease, if

the lease term

reflects the Company exercising the option to terminate. Variable lease

payments

that do

not

depend on an index or

a rate are

recognised

as expenses

(unless

they are

incurred

to

produce

inven-tories)

in the

period

in which

the event or condition

that

triggers the

payment

occurs.

In calculating the

present

value of lease

payments,

the

Company

uses its

incremental borrowing rate at

the lease

commencement

date

because the

interest rate implicit

in the lease is not readily determinable. After

the commencement

date,

the amount

ot lease liabilities is

increased to reflect the accretion of interest and reduced for

the lease

payments

made,

In

addition,

the carrying amount ot lease liabilities is remeasured

if there is a modification, a change in

the

lease

term, a change

in the lease

payments (e.9.,

changes to future

payments

resulting from

a change

in

an

index

or rate used to determine

such

lease

payments)

or a

change

in the

assessment of an option to

purchase

the underlyang asset.

The Company's lease liabilities are included in financial liabilities.

iii) Short-term

leases

and

leases

of

low-value

assets

The Company applies the short-term lease recognition exemption to its

short-term leases

(i.e.,

those leases that have

a lease

term of

12 months

or less

from

the commencement date and do not

contain a

purchase

option). It also applies

the lease of

low-value assets

recognition

exemption to leases that are considered to be low value. Lease

payments

on short-term

leases

and

leases of low-value assets are recognised

as expense on a straight-line basis over

the

lease

term.

14-

Page 10 of 33

Sunflame Enterprises Private Limited

Notes Forming Part

of the

Financial

Statements

(Amount

in t lakhs, unless otherwise stated)

CIN No. : U74899DL1984PTCO18992

k) Inventories

Inventories

are valued

at lower of cost or net realizable value.

Costs incurred

in bringing

each

product

to its

present

location

and condition are accounted for as follows:

.

Raw

materials,

packing

materials, consumables and

stores and

spares: Cost includes

cost of

purchase

and other costs

incurred in bringing

the

inventories

to their

present

location

and condition.

Cost is determined

on FIFO basis. The

materials

and other items held for use in the

production

of inventories

are not

written

down

below cost if the finished

products

in which

they will be

incorporated

are expected to

be

sold

at or above cost,

.

Finished

goods

and work in

progress:

Cost includes cost of

direct materials

and labour and a

proportion

of manufacturing

overheads based on

the

normal

operating capacity, but excludes

borrowing costs.

Cost is determined

on FIFO basis.

.

Traded

goods:

Cost includes cost of

purchase

and other costs incurred

in bringing

the inventories to

their

present

location

and condition. Cost is determined on FIFO basis.

Net realisable value is the

estimated selling

price

in

the ordinary

course of

business, less estimated

costs of completion

and

the estimated costs necessary to make

the sale,

I) Impairment of non-financial

assets

The Company assesses, at each

reporting

date, whether

there is an indication

that an asset may

be impaired, If

any indication

exists, or

when

annual

impairment

testing for an asset is

requiied, the

Company estimates

the asset's recoverable

amount. An

asset's recoverable amount is the higher

of an asset's or cashgenerating

unit's

(CGU)

fair value less cosLs

of disposal

and its

value

in

use.

Recoverable

amount is determined for

an

individual

asset,

unless the asset

does not

generate

cash inflows

that

are largely

independent

of those from other assets

or Company's assets. Where

the carrying

amount of an

asset or CGU

exceeds

its recoverable amount, the

asset

is

considered impaired

and is written

down to its recoverable

amount.

In assessing value in use, the estimated future

cash flows are

discounted to their

present

value using a

pre-tax

discount rate

that

reflects current market assessments

of the time value

of money and the risks

specific to the asset.

In determining

fair

value less costs of disposal, recent market

transactions are

taken

into

account. If no

such transactions can

be identified,

an

appropriate

valuation model

is used. These calculations

are corroborated

by valuation multiples,

quoted

share

prices

for

publicly

traded companies or other

available fair

value

indicators.

For assets excluding

goodwill,

an assessment is made

at each reporting

date to determine whether

there is an

indication that

previously

recognised impairment

losses no longer

exist or have decreased.

If such indication

exists, the

Company estimates

the asset's

or

CGU's

recoverable

amount. A

previously

recognised

impairment

loss is reversed only if

there has been

a change

in the assumptions used to determine

the asset's

recoverable

amount since the

last

impairment

loss

was

recognised.

The

reversal

is limited

so that the carrying amount of

the asset does not

exceed

its

recoverable

amount, nor exceed

the carrying

amount

that would have

been determined, net of depreciation,

had no impairment

loss been recognised

for the

asset in

prior

years.

Such reversal is recognised in

the Statement of Profit

and Loss unless

the

asset

is carried at

a

revalued

amount.

in

which case, the reversal is treated

as a

revaluation

increase.

m) Provisions

A

provision

is recognised when

the Company has

a

present

obligation

(legal

or constructive)

as a

result

of

past

event, it is

probable

that an outflow of resources

embodying economic benefits

will be required

to settle the obligation

and

a

reliable

eslimate

can be made of the

amount of the obligation.

The amount

recognized

as a

provision

is the best

estimate of the consideration

required

to settle the

present

obligation at

the

end

of the rep-orting

period,

taking into account the risks

and uncertainties

surrounding the obligation. When

a

provision

is

measured using the cash flows estimated

to s.ttle the

present

obligation, its c-arrying

amount is the

present

vilue

of those

cash flows

(when

the effect oFthe time value of money is

material).

If the effect of the time value of money is material,

provisions

are discounted using

a current

pretax

rate

that reflects, when

appropriate, the risks specific

to the

liability.

When discounting

is used, the increase in

the

provision

due to the

passage

of

time

is recognised

as a finance cost.

Contingent laabilaties

A contingent liability is a

possible

obligation

that arises from

past

events whose

existence

will

be confirmed

by the occurrence

or non-occu[rence of one or more

uncertain

future

events beyond

the control of the

Company or a

present

obligation

that is

not

recognised because it is not

probable

that an

outflow of resources will

be required to settle

the obligation. A

contingent

liability also arises in extremely rare

cases,

where

there is a liability

that cannot be recognised

because it

cannot be measured

reliably,

The

Company does not recognize

a

contingent

liability but discloses

its existence in

the

financial

statements

unless

the

probability

of outflow of resources is

remote. Provisions,

contingent

laabilities, contingent assets

and commitments

are

reviewed

at each Balance

Sheet date.

I

)'t:

Page 11

of 33

Sunflame

Enterprises Private Limited

Notes Forming

Part

ofthe

Fanancial

Statements

(Amount

in < lakhs, unless otherwase

stated)

CIN No. : U74899DLl984PTCO18992

n)

Employee benefits

Short term employee benefits

All

employee

benefits expected to

be settled

wholly within

twelve months

of rendering

the service are classified as

short-term

employee

benefits.

When

an employee has rendered

service to

the Company during an

accounting

period,

the Company

recognizes the undiscounted amount of

short-term employee benefits expected

to be

paid

in

exchange for that service as

an

expense unless another

Ind

AS requires or

permits

the inclusion of the benefits in

the cost of an asset.

Benefits such as

salaries,

wages

and

short-term

compensated absences and

bonus etc. are recognized in

Statement oF Profit

and

Loss

in the

period

in which the employee renders

the

related

service.

Defined

contribution

schemes

Contributions

to defined contribution

schemes such as

provident

fund,

employees'state insurance,

labour welfare fund

etc. are

charged as an expense based on

the

amount

of contribution required

to be made as and when

services are rendered by

the

employees.

The

Company has no obligation, other

than the contribution

payable

to the fund towards

such schemes. The

Company

recognizes

contribution

payable

as an expense, when

an employee renders

the

related

services, If

the contribution

payable

to scheme for service received before

the

Balance

Sheet date

exceeds the contribution

already

paid,

the deficit

payable

to the scheme is recognised as liability after

deducting the contribution

already

paid.

If the

contribution already

paid

exceeds the contribution due

for

services received before

the Balance Sheet date,

then excess recognised

as an asset to

the

extent that

the

prepayment

will

lead to, for example, a reduction in

future

payment

or a cash refund.

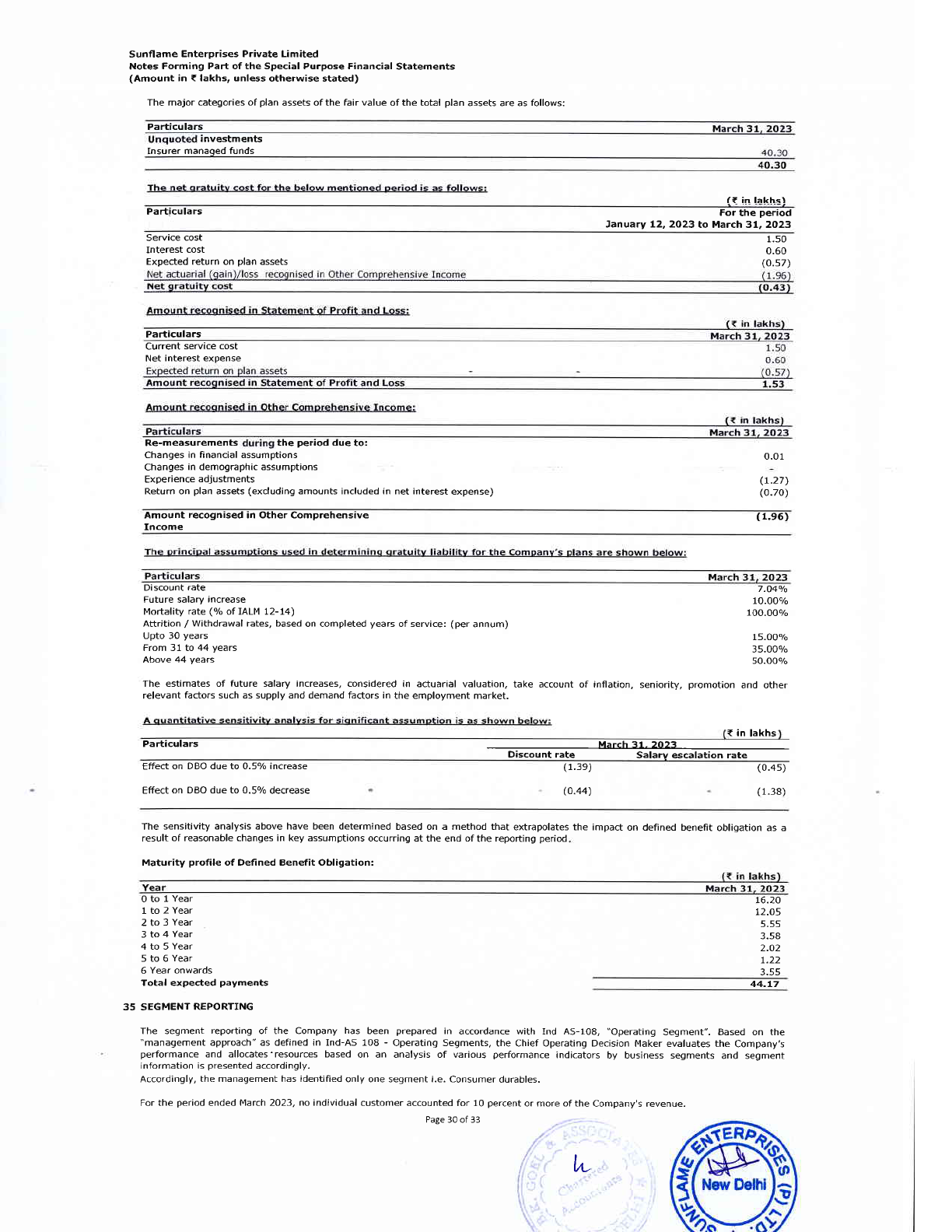

Defined benefit scheme

The

Company

operates a defined

benefit

gratuity plan

in India, which

requires

contributions to be made

to a separately

administered

fund maintained with

Life Insurance Corporation

of India. The cost of

providing

benefits under

the defined benefit

plan

is determined using the

projected

unit credit method.

Re-measurements, comprising of actuarial

gains

and losses,

the effect

of

the asset ceiling,

excluding amounts included

in net

interest on

the net

defined benefit liability and the return

on

plan

assets

(excluding

amounts included in net interest

on the net

defined

benefit liability),

are

recognised

immediately in

the

Balance

Sheet with a

corresponding debit or

credit to

retained

earnings through

OCI in

the

period

in which they occur. Re-measurements

are not reclassified

to

Statement of

Profit

and Loss

in subsequent

periods.

Past service costs are

recognised

in

Statement of

Profit

and Loss on the

earlier of:

.

The date of the

plan

amendment or curtailment,

or

.

The date that the Company recognises related restructuring

costs

Net interest is calculated by applying

the discount rate to the net

defined benefit liability

or asset. The Company recognises

the

following changes

in

the net defined benefit

obligation as an expense in

the Statement of Profit

and

Loss:

.

Seruice

costs comprising

current service costs,

past-service

costs,

gains

and losses on curtailments

and non-routine

settlements;

a nd

.

Net interest expense or income

Compensated

absences

Accumulated leave,

which

is expected

to be utilized within the next 12

months, is treated as

short-term employee benefit.

The

Company

measures

the expected cost of such absences

as the additional

amount that it expects to

pay

as a result of

the

unused

entitlement that has accumulated

at the reporting date.

The Company

treats accumulated leave

expected to be

carried forward beyond

twelve

months,

as long-term

employee benefit

for measurement

purposes.

Such

long-term compensated absences

are

provided

for based

on the actuarial valuation

using the

projected

unit

credit

method

at the

year-end,

Actuarial

gains

/

losses are immediately

taken to the

Statement of Profit

and

Loss and are not deferred. The

Company

presents

the leave as a current liability in

the

Balance

Sheet,

as the Company

believes

that it does not have an

unconditional right to defer

its settlement for 12 months

after the reporting date.

o)

Financial instruments

A financial

instrument is

any contract that

gives

rise

to a financial asset of

one entity and a financial liability

or equity

instrument of another entity.

Financial

assets

Initial

recognition and

measurement

Financial assets are classiFied, at initial

recognition, as

subsequently measured at amortised

cost, fair value

through other

comprehensive

income

(OCI),

and fair value

through

profit

or loss.

L

Page

12 of 33

sunflame Enterprises

Private Limated

Notes Forming

Part

of the

Financial

Statements

(Amount

in {

lakhs, unless otherwise stated)